While debate continues around land access and groundwater contamination, the coal seam gas industry in Queensland is powering ahead in a race for ‘first gas’. Which begs the question, why the rush?

It is no secret that government is a few steps behind the resource companies in terms of providing a solid regulatory framework for the industry to operate within. This is particularly the case for the management of CSG water in river catchments already plagued by their own water management issues (although DERM has released a CSG Water Management Policy and is investigating other beneficial use options).

Making substantial investments ahead of certain regulatory obligations appears a risky move on the part of the gas companies. After all, the gas will still be under your lease if you wait for some policy certainty, and sunk investments will provide substantial bargaining power to government to expand their wish-list as they finalise their policies. You won’t walk away from a billion dollar investment because the government makes you spend a little extra on over-the-top sweeteners to local communities.

The frantic pace of investment can be explained by the strategic first-mover advantages on offer to the winner of the race to produce ‘first gas’. British Gas’s Australian subsidiary QGC is a current favourite to win this race (to have their 'first gas' first), although Santos is a contender.

Stanford professors Lieberman and Montgomery published a defining article on first-mover advantage back in 1987 (ironically gaining a type of early-mover advantage on the study of first-mover advantages). They addressed the conditions under which such advantages are likely to exist, and we can use the ideas from their paper to better understand the advantages from winning the race for first gas.

Preemptive investment in plant and equipment

The first mover, or even second mover, to begin construction of pipeline and plant will gain a huge negotiating advantage during the expected consolidation of the sector; especially if the pipeline(s) is designed with surplus capacity. The owner of the first pipeline(s) can offer gas transport to other firms for less than the cost of constructing a their own pipeline. Once these first pipelines are operational, the sector will bargain a solution to avoid further uneconomical duplication, but there will be a balance of power in these negotiations to the pipeline owners.

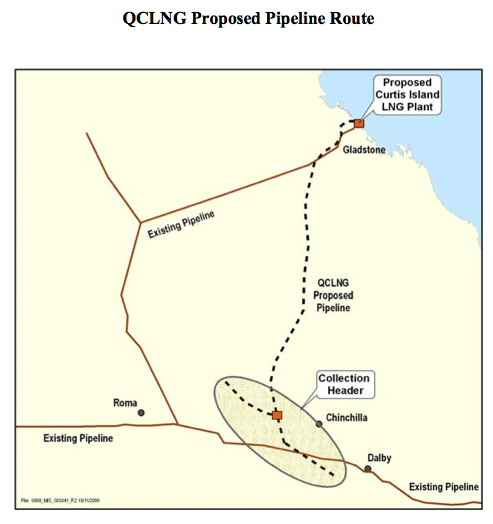

QGC’s bargaining power was significantly enhanced by last year’s approved 15 year no-coverage declaration of its proposed pipeline from the Surat Basin to Curtis Island (see map below). This approval means that the pipeline cannot be declared for open access (which would oblige QGC to provide other gas companies access to the pipeline at a regulatory price) during this period, giving it the security to invest. QGC argued (quite rightly) that the pipeline would be economic to duplicate, and that access would not be in the public interest. But only two pipelines appear economical for the expected production of the area, so there will be second mover advantages as well.

But QGC’s no-coverage declaration also added significant extra time pressures, since the approval will lapse after three years if the pipeline is not constructed and in use. Santos noted in its submission to the National Competition Council in April 2010 that QGC is unlikely to meet that three year deadline, and hence their pipeline may not be protected from a regulatory access regime. The pressure is on for QGC:

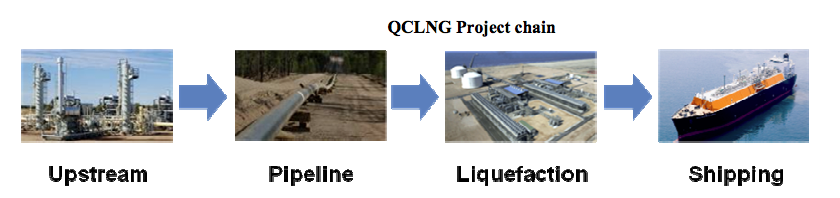

Consolidation of the sector is also likely to occur in other parts of the production chain (see below), including upstream exploration and drilling, and in particular the liquefaction stage on Curtis Island where the industry is likely to negotiate a more efficient option than the four separate plants:

Overall, the sector may consolidate extraction rights themselves by a number of means. The first mover (to construct a pipeline and plant) may buy out other tenements from a strong bargaining position, or perhaps partnerships and joint ventures will emerge with other gas producers, or even straightforward private arrangements for utilising the first mover’s pipeline and plant.

If QGC and Santos build pipelines and plant with excess capacity, they can take a share of rents from other gas companies through these types of consolidations, which is publicly their intention:

The $35 billion Australia Pacific LNG (APLNG) joint venture will theoretically become neighbours with BG, Santos/Petronas and Shell, which have all announced plans to build separate plants on Curtis Island, off Gladstone, in Queensland.However, consolidation is expected in the sector.

Switching costs and buyer choice under uncertaintyFinally, the leaders of the race for first gas will have greater opportunity to monopolise contract negotiations, and develop strong buyer relationships. The typically long contracts in the gas market reinforce the dominant position of first movers. Santos, for example, currently has a 20 year contract with Petronas, while QGC has a 20 year contract to supply CNOOC, a Chinese state-controlled oil producer.

As a final note, the pace of development is important financially simply by bringing forward returns on a multi-billion dollar investment.

So how do you get a first-mover advantage? Lieberman and Montgomery suggest the following:

A firm gains first-mover opportunities through some combination of proficiency and luck. Various types of proficiency may be involved, including technological foresight, perceptive market research, or skillful product or process development.

I would add strong relationships with government officials, which can help push through approvals ahead of the pack, and often ahead of the formation of government policy.

Overall, the sector may consolidate extraction rights themselves by a number of means. The first mover (to construct a pipeline and plant) may buy out other tenements from a strong bargaining position, or perhaps partnerships and joint ventures will emerge with other gas producers, or even straightforward private arrangements for utilising the first mover’s pipeline and plant.

If QGC and Santos build pipelines and plant with excess capacity, they can take a share of rents from other gas companies through these types of consolidations, which is publicly their intention:

“BG Group now has the strategic advantage of being the first to make a financial decision, with construction of its project to begin immediately.Given this likely eventuality, other players have pushed through with plans of their own to stay in the race for the top two, given the payoff for success is so great:

Consolidation in the CSG and LNG sector in Queensland is widely expected, and as the “first mover”, BG will be one of the main players with whom other hopefuls will now want to talk.” (here)

The $35 billion Australia Pacific LNG (APLNG) joint venture will theoretically become neighbours with BG, Santos/Petronas and Shell, which have all announced plans to build separate plants on Curtis Island, off Gladstone, in Queensland.However, consolidation is expected in the sector.

Switching costs and buyer choice under uncertaintyFinally, the leaders of the race for first gas will have greater opportunity to monopolise contract negotiations, and develop strong buyer relationships. The typically long contracts in the gas market reinforce the dominant position of first movers. Santos, for example, currently has a 20 year contract with Petronas, while QGC has a 20 year contract to supply CNOOC, a Chinese state-controlled oil producer.

As a final note, the pace of development is important financially simply by bringing forward returns on a multi-billion dollar investment.

So how do you get a first-mover advantage? Lieberman and Montgomery suggest the following:

A firm gains first-mover opportunities through some combination of proficiency and luck. Various types of proficiency may be involved, including technological foresight, perceptive market research, or skillful product or process development.

I would add strong relationships with government officials, which can help push through approvals ahead of the pack, and often ahead of the formation of government policy.

This regulatory relationship is clearly a real concern. Santos has cautioned against regulatory interference in the expected industry consolidation process, through, for example, unpredictable outcomes of no-coverage applications, given the massive impact it will have on bargaining power between gas companies. Favourable treatment in such deliberations is a true source of industry power.

I am not a gas industry insider and there may very well be some subtle considerations I have overlooked. But on the surface, the evidence is strong that the pace of development, beyond the pace of development of environmental regulation for CSG production, is being primarily driven by the race for first gas.

This means there is a trade-off between the pace of development, and the quality of the development these environmental regulations. A slower pace of development may provide incentives to better optimise investment for the industry as a whole (rather than the first mover), and opportunities for the communities affected by the industry’s development to better understand what is happening before having their input into policy making.

This leads to another question, would eliminating advantages to the first-mover slow development to allow regulation to catch up?

This is not as simple as it might sound. The threat of open access declarations could have the exact reverse effect of completely rendering the pipeline unviable. Of course, government could simply build one and charge a fixed rate of return charge to all gas companies. I wouldn’t, however, expect the operation of this pipeline to be particularly efficient, and it would still lead to lobbying by the industry players over the operation of the government’s access regime.

A creative solution might be to regulate against exporting LNG from Curtis Island until a date sufficiently late for all companies to be contenders for completing their proposed pipeline and plant. Perhaps this will encourage consolidation of the sector prior to gas being delivered. But in all honesty, I can’t think of a way to eliminate the race, without eliminating some of the benefits of CSG development, and without picking winners.

Maybe the simple solution is for government to take a hard line when it matters, such as during assessment of environmental impact statements, and incur some delays at that point for the sake of nudging trade-offs in favour of the wider community. Delaying approvals at early stages may have provided the time to collect better data about the geology and underground hydrological effects of CSG extraction.

I personally believe CSG development can be a great benefit to Queensland and Australia over the next quarter of a century, but the political class being targeted by industry lobbying needs to be aware that their hard hat photo opportunities and premature approvals are inherently trading off benefits between external stakeholders and late entrants, and the industry’s first mover(s).

I am not a gas industry insider and there may very well be some subtle considerations I have overlooked. But on the surface, the evidence is strong that the pace of development, beyond the pace of development of environmental regulation for CSG production, is being primarily driven by the race for first gas.

This means there is a trade-off between the pace of development, and the quality of the development these environmental regulations. A slower pace of development may provide incentives to better optimise investment for the industry as a whole (rather than the first mover), and opportunities for the communities affected by the industry’s development to better understand what is happening before having their input into policy making.

This leads to another question, would eliminating advantages to the first-mover slow development to allow regulation to catch up?

This is not as simple as it might sound. The threat of open access declarations could have the exact reverse effect of completely rendering the pipeline unviable. Of course, government could simply build one and charge a fixed rate of return charge to all gas companies. I wouldn’t, however, expect the operation of this pipeline to be particularly efficient, and it would still lead to lobbying by the industry players over the operation of the government’s access regime.

A creative solution might be to regulate against exporting LNG from Curtis Island until a date sufficiently late for all companies to be contenders for completing their proposed pipeline and plant. Perhaps this will encourage consolidation of the sector prior to gas being delivered. But in all honesty, I can’t think of a way to eliminate the race, without eliminating some of the benefits of CSG development, and without picking winners.

Maybe the simple solution is for government to take a hard line when it matters, such as during assessment of environmental impact statements, and incur some delays at that point for the sake of nudging trade-offs in favour of the wider community. Delaying approvals at early stages may have provided the time to collect better data about the geology and underground hydrological effects of CSG extraction.

I personally believe CSG development can be a great benefit to Queensland and Australia over the next quarter of a century, but the political class being targeted by industry lobbying needs to be aware that their hard hat photo opportunities and premature approvals are inherently trading off benefits between external stakeholders and late entrants, and the industry’s first mover(s).

{kind=link}

{kind=link}