RBA Governator Glenn "I''l be back - with higher interest rates" Stevens has been softening up the public for his next interest rate move. He warns that his toolkit contains only a blunt instrument, and we will all be affected. I guess if the only tool you have is a hammer, every problem looks like a nail.

... we only have one set of interest rates for the whole Australian economy; we do not have different interest rates for certain regions or industries. We set policy for the average Australian conditions. A given region or industry may not fully feel the strength or weakness in the overall economy to which the Bank is responding with monetary policy. In fact no region or industry may be having exactly the ‘average’ experience. It is this phenomenon that people presumably have in mind when they refer to monetary policy being a ‘blunt instrument.

I think poor old Glenn is taking his hammer to a screw.

While he wisely notes we have one set of interest rates, not one interest rate, he seems to ignore the fact that differentiation of interest rates on debt should reflect the risk for each particular loan. The problem for the RBA is that those who actually lend in the marketplace are failing to properly price the risk premium associated with their particular loans. Housing is surely a risky investment at the moment, yet interest rates do not reflect the risk premium.

The obvious alternative to shifting the whole set of interest rates is to better manage the risk premium rate for a particular industry of concern, or forcefully adjust risks taken with other measures to suit the rates adopted in that industry.

For example, if banks insist on lending for housing at relatively low interest rates, they can reduce risk by keeping lower LVRs and more conservative income estimates. If they won’t do it voluntarily, because they suffer from extreme moral hazard associated with guaranteed government bail-outs, maybe the RBA can seek to have banks better regulated with regards to housing loan risks, particularly qualifying income and LVRs.

At the moment increasing interest rates will simple increase the interest burden on current debts, high risk or not, decrease take up of borrowing for productive purposes, and fail to curb the mispricing of risk and crude lending criteria of housing loans with the major banks.

Sunday, September 26, 2010

Thursday, September 23, 2010

What I have found interesting lately

Bizarre findings in advertising:

“...in a relaxed situation like TV watching, attention tends to be used mainly as a defence mechanism. If an ad bombards us with new information, our natural response is to pay attention so we can counter-argue what it is telling us. On the other hand, if we feel we like and enjoy an ad, we tend to be more trustful of it and therefore we don't feel we need to pay too much attention to it.

"The sting in the tail is that by paying less attention, we are less able to counter-argue what the ad is communicating. In effect we let our guard down and leave ourselves more open to the advertiser's message.

"The findings suggest that if you don't want an ad to affect you in this way, you should watch it more closely."

Responsible lending?

Genworth’s acting chief executive Paul Caputo said yesterday the group had relaxed its view on earnings from overtime and second jobs in loan serviceability calculations...

Caputo said: “We support loans up to 95 per cent LVR. One of the lessons of the global financial crisis is that where a borrower has skin in the game the behaviour is very different.

“I don’t think we will get back to underwriting 100 per cent LVR loans.

“Another factor is the National Credit Act. It would be hard to see how a 100 per cent LVR loan would fit into the responsible lending criteria.”

Why of course, lending 95% of inflated values to people who need second jobs and overtime pay to meet repayments on teaser mortgage rates epitomises responsible lending.

Why are German home prices so stable? It is something they aspire to. Unlike Australia, where high prices are frowned upon everywhere except in housing.

Amazing graphic on the daily activities of Americans

Helmet laws back in the headlines - a good introduction to the debate

Leading indicators for the housing market - a website tracking advertising history to give up to the minute data on vendor discounting and days on market.

In the spirit of environmental month, a short must see video on global commercial air travel. What would be an economist environmentalist view?

Tuesday, September 21, 2010

Gaming leads to unintended consequences when governments try to stimulate housing supply

Australia’s excessively priced housing gave rise to the housing shortage myth, which in turn led governments at all levels amending planning policies to allow for greater scale of development. Densification, transit-oriented development, growth corridors and other buzz words, were drip fed by property lobby groups to politicians in search of an elixir for the ailing mortgage belt voter. The media, and by extension the public, bought into this supply-side ‘solution’ to housing affordability. Very few realised the irony of the situation – a policy on housing affordability that was a gift to existing property owners and ‘land banking’ developers.

The aggressiveness of changes to planning instruments to allow for greater heights and densities, and allow fringe areas into the urban footprint, provided opportunities to profit simply from speculation on the next change to the planning scheme. For landowners it became more profitable to wait three years for the local government to update the planning scheme to allow greater density of development, than to actually develop the site.

One example, South Brisbane, epitomises this situation.

Expectations were for this pattern to continue. A landholder in this area recently mentioned they have no reason to sell or develop when the council keeps increasing the value of their land by changing the planning scheme. Landholders are gaming the Council, waiting for a signal that the gifts will soon expire before selling up to developers.

Maybe that signal is here.

The State government has intervened in the latest round of planning scheme changes to request the proposed height limits be cut back – where 12 storeys was proposed, they will allow seven.

For anyone aware of the standoff taking place the flood of development sites onto the market in the month since the State government decision would come as no surprise. Who would have thought reducing height limits would promote so much development activity?

The moral of this story is that certainty (or lack thereof) can greatly change real outcomes. Economists often foolishly assume that all government decisions are taken at face value by the marketplace. Few realise the time element and that parties affected will already be anticipating the next decision, or gambling on a political backflip.

UPDATE: More evidence of rewarding land banking rather than productive land use, from the Local Government Association of Queensland -

The aggressiveness of changes to planning instruments to allow for greater heights and densities, and allow fringe areas into the urban footprint, provided opportunities to profit simply from speculation on the next change to the planning scheme. For landowners it became more profitable to wait three years for the local government to update the planning scheme to allow greater density of development, than to actually develop the site.

One example, South Brisbane, epitomises this situation.

At this prime location, within a stone's throw of the CBD, the previous limits of 12 and eight storeys were already conservative.The planning scheme for this precinct has changed from allowing four storeys, to seven storeys, then proposing eight storeys, then twelve storeys in the latest draft plan, and now the UDIA is calling to increase the heights much further. With the approval of a 30-storey tower adjacent to Milton railway station, one could assume there is a long way to go in this saga.

Expectations were for this pattern to continue. A landholder in this area recently mentioned they have no reason to sell or develop when the council keeps increasing the value of their land by changing the planning scheme. Landholders are gaming the Council, waiting for a signal that the gifts will soon expire before selling up to developers.

Maybe that signal is here.

The State government has intervened in the latest round of planning scheme changes to request the proposed height limits be cut back – where 12 storeys was proposed, they will allow seven.

For anyone aware of the standoff taking place the flood of development sites onto the market in the month since the State government decision would come as no surprise. Who would have thought reducing height limits would promote so much development activity?

The moral of this story is that certainty (or lack thereof) can greatly change real outcomes. Economists often foolishly assume that all government decisions are taken at face value by the marketplace. Few realise the time element and that parties affected will already be anticipating the next decision, or gambling on a political backflip.

UPDATE: More evidence of rewarding land banking rather than productive land use, from the Local Government Association of Queensland -

The LGAQ today criticised a key provision of legislation introduced to state parliament on Tuesday which retained a 40 per cent rate subsidy for large companies holding big tracts of land approved for development but not yet formally subdivided.

The money at stake is not the issue here. The issue is the massive contradiction of rewarding developers for not sub-dividing land to increase supply when the state government says it is championing housing affordability issues

Sunday, September 19, 2010

Flow-on effects of recycling - are there net benefits?

It is widely claimed that recycling “saves resources.” Often, recycling proponents claim that it will save specific resources, such as timber, petroleum, or mineral ores. Sometimes particularly successful examples are singled out, such as the recycling of aluminum cans. Both of these lines of argument rest on the notion that reusing some resources means using fewer total resources.

Daniel K. BenjaminLike efficiency, the word recycling reflects positivity from all angles. How could anyone say a bad thing about recycling?

I propose not to say a bad thing for the sake of cementing my identity as a super-sceptic, but to examine in detail the potential flow-on effects of recycling and determine whether the espoused benefits can theoretically be delivered.

Generally two benefits of recycling are proclaimed. First, waste will be diverted from landfill, thus we can reduce the space required for this purposed and reduce the threat of leaching from landfill sites into groundwater systems and other environments. Second, recycled material will substitute for raw materials and thus reduce consumption of natural resources which may have associated negative environmental externalities.

These are two distinct benefits, and achieving one does not necessarily imply achieving both.

There are also two different economic scenarios for achieving recycling with different outcomes – the profitable recycling scenario, and the unprofitable recycling scenario that requires government support.

The profitable scenario represents an improvement in overall economic efficiency, thus, like the case of profitable energy efficiency, it facilitates future economic growth and improves our productive capacity.

In this scenario, recycled material cannot be said to be diverted from land fill, because it would never have been put there in the first place due to the material’s value to remanufacturing. If the material was simply dumped on the street there would be an opportunity for a business to emerge to collect the material and sell for a profit. Without a counterfactual we cannot estimate the effect on either of our two recycling claims.

If we assume instead that the counterfactual scenario is one where the technology had not yet emerged to make recycling profitable, then we can now consider the flow-on effects from the technology. It is best to have a single material in mind, say glass, when thinking of these effects.

First, the price of the final goods (windows, bottles etc) using the newly recyclable material will decline due to the reduced cost of recycled instead of raw materials. Thus we will see an increase in demand (not a shift in the demand curve, but a new point on the demand curve at a lower price) for these final goods and therefore an increase in demand for recycled and/or raw materials (recycled glass or silica from natural sand deposits). Depending on the availability of recycled material compared to the total quantity of raw materials, this can lead to greater demand for natural resource itself (sand mining).

We can now say we have probably diverted waste from landfill leading to a greater quantity of material circulating in the hands of society (as either capital equipment – glass in buildings perhaps- or soon to be recycled consumables – maybe bottles), but we cannot say with certainty that the new recycling technology has reduced demand for the particular natural resource in question. Nor can we say that demand for, and consumption of, other natural resources remains unaffected. In fact the new recycling technology, since it improved overall economic efficiency, is likely to increase demand for all natural resource inputs to the economy.

The alternate unprofitable scenario represents a decrease in overall economic efficiency, and will reduce overall economic activity compared to scenario where government did not use its coercive power to enforce this unprofitable venture.

In this scenario we are likely to see a decline in waste to landfill compared to the economically efficient situation where recycling is not subsidised. We face the same situation of compensatory demand due to price declines of final goods manufactured using the cheaper subsidised recycled materials. This scale of this offsetting behaviour cannot be readily estimated and is likely to strongly depend on the relative prices and quantities of the recycled materials and raw material inputs are a particular point in time. A decline in overall demand for raw materials in the economy as a whole is certain in the unprofitable scenario due to the overall reduction in economic efficiency.

For unprofitable recycling the net result will be a reduction in waste to landfill of both the recycled good and other goods (since we can now produce fewer goods in total across the economy), and a reduction in resource consumption of the recycled material and all other resource inputs to the economy.

In what is becoming a familiar environmental theme at this blog, it should be clear that indirect measures to curb negative environmental impacts from our activities, such as promoting conservation behaviours, profitable energy efficiency, and recycling, have questionable net impacts on the environmental issue at hand.

Returning to our two main environmental goals of recycling – reduce negative impacts form landfill sites and reduce resource extraction that involves an environmental burden – we can clearly offer more direct measures which are both easy to establish and have certain environmental benefits.

The first environmental goal can be achieved by setting minimum environmental standards for landfill sites to address leaching (or any other associated problem depending on local conditions) including, perhaps, restrictions on location. In response to these criteria, landfill operators (public or private) would need to adopt appropriate measure to limit external impacts – possibly lining their pits with impermeable material, sorting, washing or removing particular types of waste, or some other creative response. These extra costs of waste disposal – the internalised environmental cost – will flow through to the cost of disposal, and may render some recycling programs profitable.

For the second environmental concern, resource extraction, similar direct controls can be used. Sticking with the glass example, the scope of sand mining can be limited through planning controls where natural environments which are valued by the community. Once this limit is established, sand mining in that area can proceed, at any particular rate, with certainty that there is a finite limit to the environmental cost.

These limits would never be, strictly speaking, perfect. They would at best reflect the perceived value of the environment to the community. There is no reason that the limits should not be stricter in some areas than others.

As an indirect environmental measure with questionable benefits, recycling, like efficiency, is claimed to be a panacea for a variety of poorly defined environmental ills. We often forget to critically examine the link between this indirect environmental ‘remedy’, and the target environmental illness.

Friday, September 17, 2010

A closer look at Australian incomes and predictions from Google Trends

Income distribution fascinates economists. The release of the new ABS personal income estimates for small areas gives a complete picture of the geographical spread of incomes in this country for the first time. Given the amount of media attention to Australia’s recent economic success, these figures surprised me. They are extremely low. Australia’s average gross personal income for 2007/08 was $44,402 or about $853 per week.

Let’s take a closer look.

The calculation of this income figure is an average of individuals with any of the following sources of income in the 2007/08 financial year -wage and salary income, investment income, unincorporated business income, superannuation and annuity income. It does not include individuals whose sole income comprised government benefits. It therefore includes all casual, part-time and full-time workers, self-funded retirees and business owners. What it doesn’t include are the government benefits many of these groups may also receive.

If government benefits received by this group were included the average would be higher. After tax incomes would, however, be much lower.

It is important to be clear that these are gross incomes after deducting losses, remembering that there are 1.7million residential property investors with net losses in 2007/08 of $8.6billion. Averaging across the population does not clearly show the diversity of investment income and the severity of many negative investment incomes.

We must also note that these are all average numbers, and as is typical for these types of (assumed) distributions, the median income would be much lower.

Why is this important?

Much of the mainstream economic establishment has latched on to the idea that incomes have been rapidly rising in Australia, yet the data does not to support this optimistic view.

If we examine, for example, total earnings of full time employees, we can see that in the period 1995-2010, annual growth in before tax total earnings was a mere 3.9%. In real terms, a 1.3% annual increase in full time wages since 1995. Total earnings of fulltime employees in 2007/08 were $67,860 (wage plus other income), and from recent data, it looks like private sector earnings are pretty flat since then. That’s about $52,000 after tax.

The ABS capital city house price index on the other hand, rose by an annual rate of 9.4% since 2002. RPData-Rismark currently has Australia’s median dwelling price (detached and attached) at $405,000 and the ‘trimmed mean’ home price at $435,000.

Anyone who claims home prices are rising in line with incomes either has not seen the data, or is being intentionally deceptive. The RBA can be counted amongst this group.

Australia’s current housing situation is truly unsustainable. It would take two above average fulltime workers to buy one median priced dwelling. If they want to live in or near a capital city, the situation is more severe.

With an income picture less rosy than many make out, it is quite clear that current elevated house prices are not due to owner occupier demand - there is simply not enough income for that to be true. They have risen strongly through speculative investment decisions backed by government support (including negative gearing). Anyone who claims that home prices are stable due to incomes fails to realise that prices are determined by investors who can abandon the market in droves as soon as returns start looking bleak.

Moving on.

Google has an uncanny ability to predict the future. Google Trends allows users to plot search popularity over time for any search term you like. I have borrowed this idea from various other sites, but what prompted me to post it was a line I read that went something like - ‘once the mainstream media is talking about a housing bubble it is ready to crash.’ As you can see below, this was definitely true in the US. The recent attention to Australia’s precarious housing situation is a worrying sign for those recently leveraged into the market.

Tuesday, September 14, 2010

Energy efficiency - further reading

A robust discussion on the impact of energy efficiency on energy use took place in the journal Energy Policy over the decade since Len Brookes' article The greenhouse effect: the fallacies in the energy efficiency solution in 1994. It concluded (for now) with another article by Brookes in 2003 entitled Energy efficiency fallacies- a postscript. Brookes' conclusions are almost identical to my own, and those of Blake Alcott - capping or rationing resources where their use entails some kind of externality.

Brookes also adds taxing resources to reflect the cost of negative externalities, which one assumes, would be spent on reparation activities to return to a new optimal resource allocation which internalises the cost of pollution and eliminates the possibility of rebound effects (if reparations are possible).

It is worth reading his conclusions in full (below the fold):

Brookes also adds taxing resources to reflect the cost of negative externalities, which one assumes, would be spent on reparation activities to return to a new optimal resource allocation which internalises the cost of pollution and eliminates the possibility of rebound effects (if reparations are possible).

It is worth reading his conclusions in full (below the fold):

Sunday, September 12, 2010

Dutch Cargo Bike Review

Note: A follow-up (3yr) review is here. I am now a local ambassador for Dutch Cargo Bikes. If you would like to test rise this bike in Brisbane (or a three wheeler) email me at cameron@dutchcargobike.com.auI almost convinced myself not long ago that a bicycle for carrying children was a completely unjustified expense. Luckily I didn't. Because my sparkling new bakfiets.nl cargo bike, supplied through Dutch Cargo Bike, arrived several weeks ago. And I'm excited. I've also convinced myself that in reality it isn't expensive, and in fact represents great value for money.

In the past three weeks I've used the bike daily for the commute to work, to the shops, to day care, to pick up my wife from yoga – you name it. It is now time for an early review. But first, I need to explain how this value conscious economist ended up with a $3000+ bike.

For the non-cyclist the prices of these bikes can be a shock. Bikes are meant to cost hundred, and second hand cars are meant to costs thousands. We have trouble seeing where all the money goes on a bicycle! But as avid cyclists would know, high quality equipment still costs money in the world of bikes, and this bike is extremely high quality.

You need to understand that the ongoing costs for cycling are extremely low, and lower with higher quality components. I can imagine in 5 years when our youngest child is happily riding themselves we might have less use for the bike, but it would be reasonable, given the high quality of all the parts on this bike, to expect the bike to be very good condition. If the bike sold for $2000 in five years time, you are looking at a total 5 year total cost of around $1300 (including servicing, tyres etc) or less than $300 per year, or $5.70 per week –a little more than one bus fare – which is a bargain for a young family given the great health and social benefits from family cycling [1].

I believe this bike represents good value for our family, so what are my first impressions?

The Dutch Cargo Bike team arranged delivery and assembly at my local bike shop. What first struck me about the bike was the attention to detail – rubber antislip coating on the floor of the box, with a ledge for kids to use to help them climb in, a magnetic latch for the very stable four-prong kick stand (apparently a patented design by Maarten van Andel), and built in elastic straps for securing loads to the heavy duty rear rack. Not to mention the very bright generator light as standard equipment (which I now just leave on at all times).

The bike rides incredibly smoothly. In fact I can cross manoeuvrability from my cons list and shift it to the pros list. After a bit of practice you can steer this puppy easily through tight gaps, even loaded with four children. And slow, well, it’s actually not as sluggish as I expected either. After a week of riding this fairly weighty beast my legs seem to have built up the strength to ride at breakneck pace and tackle those hills that seemed so intimidating at first.

The box is extremely strong. It looks like flimsy plywood in photos, but is almost one centimetre think, does not scratch easily, and does not flex under heavy loads. I've taken all my mates for a spin, and even loaded with my wife, child and dog (80kg) on board it feels solid and safe.

The most unexpected benefit of the bike is that after a laid back ride and lots of smiles and waves from passersby, you always arrive happy.

fn.[1] The alert reader will note there is an opportunity cost to the forgone $3000 that could have been alternatively invested, say at 5%, which adds another $150 per year.

fn.[1] The alert reader will note there is an opportunity cost to the forgone $3000 that could have been alternatively invested, say at 5%, which adds another $150 per year.

Wednesday, September 8, 2010

Energy efficiency: A flawed paradigm

The word efficiency carries a meaning immersed in all things positive – you never hear that being more efficient could possibly be detrimental. In fact, if you can bear the evangelical fervour, you may have read about achieving ‘Factor Four’ or ‘Factor Five’ gains in energy efficiency, as part of a ‘Natural Capital’ revolution comprising a ‘decoupling’ economic growth from a growth in the consumption of exhaustible resources – aka ‘sustainability’. You may even have heard that I=PAT, where environment impact (I) is a function of population (P), affluence (A) and technology (T), and that becoming more efficient will enable a desired level of affluence will far less environmental cost.

Believe me, this is all nonsense, and indeed counterproductive to the stated aims of curbing resource use and decreasing negative environmental externalities.

When it comes to natural resource use, and the externalities associated with resource extraction and production, efficiency alone is the enabler of greater consumption. William Stanley Jevons first noted that technological improvement, in terms of greater efficiency and therefore productivity, was the enabler of greater coal consumption in Britain back in 1865 in his book, The Coal Question: an Inquiry Concerning the Progress of the Nation, and the Probable Exhaustion of our Coal-mines. His observation was coined Jevon’s Paradox, even though the argument that technological improvements in resource efficiency (modes of economy) leads to greater resource use was already widely accepted in the labour market:

“As a rule, new modes of economy will lead to an increase in consumption according to a principle recognised in many parallel instances. The economy of labor effected by the introduction of new machinery throws labourers out of employment for the moment. But such is the increased demand for the cheapened products, that eventually the sphere of employment is greatly widened.”

Monday, September 6, 2010

Economist forecasts for the record

Just for fun here are some recent forecasts from some of Australia’s leading economists.

Bill Evans – Westpac Chief Economist - 3 September 2010

At present we are expecting rates to rise by 75 basis points during 2011. Markets will need to adjust a long way to accommodate that view

Peter Jolly – NAB Head of Global Research - 4 September 2010

Our year ended GDP forecast has lifted to 3¼% from a little under 3% As a consequence, we debated whether the 100bps of tightening in our forecast starting February 2011 was enough. We think it is, but it did remind us that a 2010 hike remains possible should either a) Q3 inflation in late October be shockingly high or b) the economy grows above trend in the 2nd half and the unemployment rate (now 5.3%) plunges through 5% - quite possible

Christopher Joye – Rismark - 23 Aug 2010

The economy is about to embark on a period of above-trend growth (mean of the ABS trend measure since June 2000 is 0.7%/qtr or 0.4%/qtr/capita)

Warren Hogan – ANZ Chief Economist - 1 September 2010

The consensus seemed to be that the Reserve Bank will be happy to sit pat for six months and then raise rates by 100 basis points through next year. The ANZ's Warren Hogan was the hawkish outlier of the group, predicting 150 or 170 points over the next 18 months.

Hogan believes we are about to see a period of serious inflationary pressures thanks to the commodities boom's income wave – the CBA's Michael Blythe reckons the income surge will add 3 or 4 per cent to GDP over the next couple of years

Dr Frank Gelber – BIS Shrapnel Chief Economist - 7 September 2010

Interest rates are set to rise and commercial property values will skyrocket.

"I've never seen a lower risk, higher prospective return, in the commercial property market, ever," he said. "We're looking at rents and property values doubling in Sydney and Melbourne over the next five years." [commercial property]

Cameron Murray –Economist, blogger (you read it here first)

Inflation and GDP will surprise on the low side in the September quarter. Remember, the June quarter had a booming terms of trade (which is now languishing), fiscal stimulus (which is now finished) and two interest rate moves by the RBA which could drain consumer confidence and spending, especially when combined with house price nerves and debt concerns. Therefore I expect the RBA to keep rates on hold for the next 6 months (with some independent upward moves of mortgage rates by banks), with a possible stimulatory move by the RBA next year.

On a different note, for those who want a little more insight into Australia’s own residential mortgage backed securities market, this piece from Adam Dellaverde might pique your curiosity.

Sunday, September 5, 2010

Waste Revisited – the ‘Green’ bag revolution

The last time I wrote about waste I started like this:

The oft-repeated mantra of the ‘ecological modernist’ is that we are wasteful. They see the rise of disposable cups, packaging and plastic bags as a sign that of that wastefulness. Further, in terms of energy and climate change, they see traffic jams full of cars with only the driver inside, and lights on in buildings with no occupants in the city all night – a society squandering our resources. If only we could stop all this wastefulness and build a utopia.

I argued that waste is a relative and value driven term, and that the popularity of waste as a concept in environmental circles is in fact slowing progress on environment issues, as it distracts from the core problems.

Waste is not a useful concept, but litter, ‘stuff in the wrong place which may cause harm’, certainly is. Governments have waged war against plastic bags in the name of reducing litter (even though they prefer the term waste).

Outlawing giveaway plastic bags appears to have gained traction with policy makers as one path to environmental bliss. South Australia has a law. Victoria has one. Ireland has one (although the list of exemptions is pretty long). California is considering one. And the list goes on.

Thursday, September 2, 2010

The Environment Revisited

I want to revisit some of the key environmental themes of this blog that have had very little airtime lately. In particular I want to revisit, over the next month, the unintended consequences of some of our favourite environmental policies and personal choices.

For those new to the blog, the divergence of post topics from my blog title is explained here:

...understanding property is the key to a reasoned approach to preserving our quality of life by preserving environmental amenity. Maybe I am more of a ‘quality of life’ economist who believes there are many non-market goods, including the quality of, and accessibility of natural environments, that are major contributors to our well-being.

However the increasing fanaticism I have observed in some areas of the climate change movement, the lack of ability for some environmentalists to see the forest for the trees (pun intended), has lead me to distance myself from some of the core environmentalist views.

As a rule of thumb I believe we should first focus our efforts on local, tractable environmental problems with clear externalities, and implementable solutions – protecting diversity and fish stocks in the Great Barrier Reef, tackling air pollution and improving urban amenity, and preserving the quality of waterways and wilderness areas. Climate change, that global intractable problem, has dropped down my list of concerns, even though my previous research focussed on ways to reduce greenhouse gas emissions.

The development of my ideas on the environment is the reverse of renowned ‘skeptical environmentalist’ Bjorn Lomborg’s u-turn. He once held a strong position that climate change was far down humanities list of concerns, particularly noting the obvious an immediate threats from treatable diseases in the developing world. Now climate change to the top of his list, no doubt to pitch his new book to cashed-up fanatics.

My second rule of thumb is that personal ‘green’ consumption choices make no difference, and small actions do not add up. These behaviours are typically offset by other economic adjustments in upstream production and by choices of others as prices respond. These effects are know an rebound effects.

A recent article in The Economist highlights new research showing these rebound effects in action. The study estimates that new energy efficient lighting technology will increase energy consumption in the long run. My own research showed that conservation behaviour, such as using lights and electrical appliances and driving less, will also result in minimal change as money saved get spent elsewhere in the economy.

I intend to revisit ideas about waste, efficiency, environmental taxes, recycling and solar power over the next month to see how my ideas have developed, and to seek input to develop them further.

For those new to the blog, the divergence of post topics from my blog title is explained here:

...understanding property is the key to a reasoned approach to preserving our quality of life by preserving environmental amenity. Maybe I am more of a ‘quality of life’ economist who believes there are many non-market goods, including the quality of, and accessibility of natural environments, that are major contributors to our well-being.

However the increasing fanaticism I have observed in some areas of the climate change movement, the lack of ability for some environmentalists to see the forest for the trees (pun intended), has lead me to distance myself from some of the core environmentalist views.

As a rule of thumb I believe we should first focus our efforts on local, tractable environmental problems with clear externalities, and implementable solutions – protecting diversity and fish stocks in the Great Barrier Reef, tackling air pollution and improving urban amenity, and preserving the quality of waterways and wilderness areas. Climate change, that global intractable problem, has dropped down my list of concerns, even though my previous research focussed on ways to reduce greenhouse gas emissions.

The development of my ideas on the environment is the reverse of renowned ‘skeptical environmentalist’ Bjorn Lomborg’s u-turn. He once held a strong position that climate change was far down humanities list of concerns, particularly noting the obvious an immediate threats from treatable diseases in the developing world. Now climate change to the top of his list, no doubt to pitch his new book to cashed-up fanatics.

My second rule of thumb is that personal ‘green’ consumption choices make no difference, and small actions do not add up. These behaviours are typically offset by other economic adjustments in upstream production and by choices of others as prices respond. These effects are know an rebound effects.

A recent article in The Economist highlights new research showing these rebound effects in action. The study estimates that new energy efficient lighting technology will increase energy consumption in the long run. My own research showed that conservation behaviour, such as using lights and electrical appliances and driving less, will also result in minimal change as money saved get spent elsewhere in the economy.

I intend to revisit ideas about waste, efficiency, environmental taxes, recycling and solar power over the next month to see how my ideas have developed, and to seek input to develop them further.

Wednesday, September 1, 2010

Interpreting today's National Accounts

A cautionary tale from RMIT's Dr Steven Kates over at Catallaxy Files:

Three sets of figures stand out as part of a cautionary tale told by the numbers.

The first is the set of figures on Private Gross Fixed Capital Formation, the data on private sector investment. Across the year the growth rate was a quite sedate 1.3% and for the quarter itself (I always use the trend numbers), the growth rate was actually negative, coming in at -0.1%.

Meanwhile, for Public Gross Fixed Capital Formation the growth rate was 38.5%, a monstrous increase. The quarterly figure was only 4.7% which means the numbers are coming back down to sane proportions but even so.

Then thirdly there is the figure for imports which rose by 15.9% across the year, raising spectres of its own. For the quarter it was 1.9%, and for the first time this financial year was lower than the level of exports.

There is a story of debt printed all over the accounts, both domestic and foreign. We have as a nation splurged to get a result, but the costs are still to be paid.

The notion of a double dip, especially after efforts made to maintain the appearance of growth in an economy heading into recession, is in part due to the need not only to unpick the production errors that led to recession in the first place, but now to undo all of the structural changes introduced as part of the stimulus. People producing and installing pink batts now have to find a real job although the major horrors may take place in the United States. We shall see what happens then.

Monday, August 30, 2010

Competition Series Part IV: The future

While competition can clearly bring significant consumer benefits (think Virgin Blue and the airline shake up, or Aldi and current supermarket competition) the evidence is clear that this is not always the case, and that harnessing the innovation stimulated by competition can come with a large coordination cost.

One major consideration as to whether competition can work effectively – will government still control a production bottleneck?

For example, once airport runways are operating at capacity, the government will have the final say on approving new runways. In the mean time, airport owners can act as a monopoly as there is a huge, in fact insurmountable, barrier to entry.

Thursday, August 26, 2010

Friday quick links

On personal freedoms, litigation, and common sense (a good read)

Did he really say that? Chris Joye, optimist, reckons that stability and continuity are valuable things for an economy that is hesitantly emerging from the global financial crisis and about to embark on a period of above-trend growth

Does light rail improve public health? This study has results showing obesity declining in areas serviced by light rail in a before and after comparison.

In the spirit of the competition series running this month I thought it opportune to comment on Sam Wylie’s recent article on reciprocal obligations of banks following government support. Thinking about the whole story makes the situation seems ridiculous. The government privatises the banking system, allowing privately owned businesses to determine the money supply, and then bails them out after a crash which resulted from their undue risk taking, then left them to go on their merry way to make abnormally high profits once again. Clearly, there is no moral hazard here and this wonderful situation is highly beneficial for the people.

Can you draw a conclusion about the impact of population growth on economic welfare from this graph?

Did he really say that? Chris Joye, optimist, reckons that stability and continuity are valuable things for an economy that is hesitantly emerging from the global financial crisis and about to embark on a period of above-trend growth

Does light rail improve public health? This study has results showing obesity declining in areas serviced by light rail in a before and after comparison.

In the spirit of the competition series running this month I thought it opportune to comment on Sam Wylie’s recent article on reciprocal obligations of banks following government support. Thinking about the whole story makes the situation seems ridiculous. The government privatises the banking system, allowing privately owned businesses to determine the money supply, and then bails them out after a crash which resulted from their undue risk taking, then left them to go on their merry way to make abnormally high profits once again. Clearly, there is no moral hazard here and this wonderful situation is highly beneficial for the people.

Can you draw a conclusion about the impact of population growth on economic welfare from this graph?

Tuesday, August 24, 2010

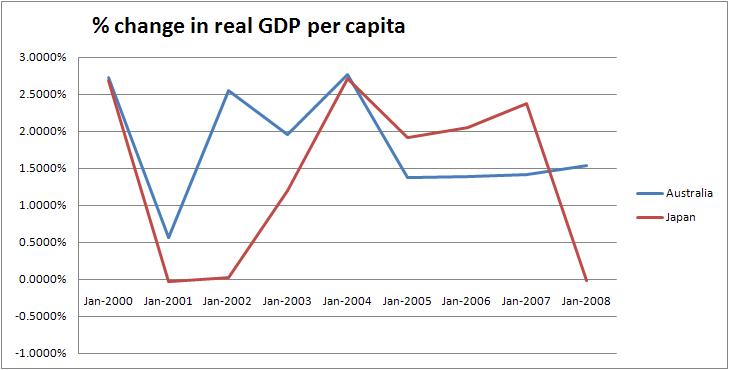

What does it mean for an economy to ‘turn Japanese’ and what determines whether it will?

What few seem to appreciate, either inside or outside of Japan, is just how strong the resulting Japanese recovery from 2002-2008 was. It was the longest unbroken recovery of Japan’s postwar history, and, while not as strong as pre-bubble Japanese performance, was in fact stronger than the growth in comparable economies even when fuelled by their own bubbles.

How on Earth did Japan manage that with their ageing population and zero population growth? Indeed, Japan outperformed Australia in productivity growth since 2000 and very nearly kept pace with real GDP per capita growth.

The RBA’s Ric Battelino seems confused. In a recent speech on the Australian economy he notes that “the slowdown in productivity growth has meant that GDP growth in the latest decade was not as fast as in the previous decade”, while also saying that for the past two decades “part of the growth came, of course, from the fact that the population grew strongly over the period, particularly in recent years.” What? The data he presents shows a negative correlation between economic growth and population growth, yet he continues to promote a positive relationship.

Australia’s average annual real growth in GDP per capita (currently the best measure of economic performance) since 2000 is 1.28%. While I can’t find a direct measure from the Japanese Statistical agency, using the World Bank data collection I can make a comparison of real GDP growth per capita of Australia and Japan using a common methodology. Using these statistics I find that Australia had a mean annual growth in real GDP per person since 2000 of 1.8% while Japan’s was 1.4%.

How on Earth did Japan manage that with their ageing population and zero population growth? Indeed, Japan outperformed Australia in productivity growth since 2000 and very nearly kept pace with real GDP per capita growth.

The RBA’s Ric Battelino seems confused. In a recent speech on the Australian economy he notes that “the slowdown in productivity growth has meant that GDP growth in the latest decade was not as fast as in the previous decade”, while also saying that for the past two decades “part of the growth came, of course, from the fact that the population grew strongly over the period, particularly in recent years.” What? The data he presents shows a negative correlation between economic growth and population growth, yet he continues to promote a positive relationship.

Australia’s average annual real growth in GDP per capita (currently the best measure of economic performance) since 2000 is 1.28%. While I can’t find a direct measure from the Japanese Statistical agency, using the World Bank data collection I can make a comparison of real GDP growth per capita of Australia and Japan using a common methodology. Using these statistics I find that Australia had a mean annual growth in real GDP per person since 2000 of 1.8% while Japan’s was 1.4%.

Sunday, August 22, 2010

Living in a bubble

Morgan Stanley’s Gerard Minack aptly uses the phrase ‘living in a bubble’ as the title of his research note about Australia’s housing market. Minack’s conclusion is that Australian housing is overvalued, but he sees prolonged stagnation rather than a dramatic pop of the price bubble - I expect that the real returns on residential investment will be negative over the next decade.

I want to highlight a few key charts from the research note. The first is a comparison of prices to rents, showing a massive increase above the long run average since 2000 (I believe this figure is price divided by annual gross rent divided by 100). One could call on interest rates as an explanation, but mortgage interest rates have actually been increasing over much of that period.

The second chart is a comparison of the value of the housing stock to household income, which further supports this claim that home prices are 30-40% above average levels.

The second chart is a comparison of the value of the housing stock to household income, which further supports this claim that home prices are 30-40% above average levels.

I want to highlight a few key charts from the research note. The first is a comparison of prices to rents, showing a massive increase above the long run average since 2000 (I believe this figure is price divided by annual gross rent divided by 100). One could call on interest rates as an explanation, but mortgage interest rates have actually been increasing over much of that period.

The next chart is one that compares the share of household debt by income level. One of the RBA’s claims has been that Australia’s housing market is stable because most debt is held by high income earners - ...our assessment is that the increase in debt has broadly been concentrated in the hands of those generally more able to service it. This is identical the the US situation in 2007.

Thursday, August 19, 2010

Helmet law research hits the headlines

Helmet laws hit the headlines with a new Australian study proclaiming their ineffectiveness at providing safety to cyclists, while in Canada the debate is heading the other way (due to this study - sorry I can't get the full text to review the methods).

The Australian study neatly controls for the number of cyclists and distance cycled by comparing the ratio of head to arm and hand injuries resulting from cycling activities from hospital records. A change in this ratio (lower head injuries per arm and hand injury) would be a clear indicator of the success of helmet wearing in preventing head injury.

The figure above shows the ratio (ICD9) from 1988 to 2000. Helmet laws were introduced in 1991, and self-reported compliance for two age groups (<16years and >16years) are plotted from 1991 to 1995.

The figure above shows the ratio (ICD9) from 1988 to 2000. Helmet laws were introduced in 1991, and self-reported compliance for two age groups (<16years and >16years) are plotted from 1991 to 1995.

The essential argument is that the large decline in the ratio of head to arm injuries occurred before the helmet law, and much before compliance with the law. In the two year period where helmet wearing took off following the legislation (1991 to 1993), the ratio dropped from 0.8 to 0.75 – hardly a success. The drop in the two years preceding the helmet law was from 1.15 to 0.8.

The author suggests that other road safety measures contributed to the decline, while the law itself would have contributed to a decline in the number of cyclists (some evidence for the decline is here) which itself made cycling more dangerous and lead to a flattening of the trend -

The reduction in numbers of people cycling may have actually increased the risk to the remaining cyclists because of Smeed’s Law and the safety in numbers hypothesis.

The Australian study neatly controls for the number of cyclists and distance cycled by comparing the ratio of head to arm and hand injuries resulting from cycling activities from hospital records. A change in this ratio (lower head injuries per arm and hand injury) would be a clear indicator of the success of helmet wearing in preventing head injury.

The essential argument is that the large decline in the ratio of head to arm injuries occurred before the helmet law, and much before compliance with the law. In the two year period where helmet wearing took off following the legislation (1991 to 1993), the ratio dropped from 0.8 to 0.75 – hardly a success. The drop in the two years preceding the helmet law was from 1.15 to 0.8.

The author suggests that other road safety measures contributed to the decline, while the law itself would have contributed to a decline in the number of cyclists (some evidence for the decline is here) which itself made cycling more dangerous and lead to a flattening of the trend -

The reduction in numbers of people cycling may have actually increased the risk to the remaining cyclists because of Smeed’s Law and the safety in numbers hypothesis.

Wednesday, August 18, 2010

The Shadow Public Service

Tyler Cowen asks: Why does anyone pay for macro-economic forecasts when they are typically wrong and in the public domain? The answer is simple. Forward planning requires some assumption about the future. One comment notes that you wouldn’t plan a military exercise without checking the weather forecast, no matter how inaccurate.

But more fundamentally, the reason for paying for such advice is due to the need to appear objective. Whether objectivity involves accuracy is a secondary concern.

Governments face this problem regularly. To avoid accusations of political influence they engage an army of external consultants to provide trivial advice that can easily be determined by internal staff. This army is the Shadow Public Service.

Oddly, critics fail to note that external advice that does not support a government position will be filtered anyway. Like a barrister in a criminal trial, they won’t ask questions they don’t already know the answer to.

I regularly deal with private economics consulting firms and can’t help but wonder how big an industry is supported by the farcical drive for an illusion of objectivity by government. I have personally engaged millions of dollars of work from private economics consulting firms for the sole purpose of having a basis for a predetermined decision that appears independent.

The final irony of it all is that the best qualified people tend to leave government departments to take on the same role as a consultant, but at five times the cost. And, of course, governments have a habit of filling vacant positions whether they are required or not. Either recruit the staff you need to provide proper advice, or get rid of them and draw upon the resources sitting in private firms. Don't waste money on a shadow public service unless they provide a real contribution beyond the objectivity illusion.

But more fundamentally, the reason for paying for such advice is due to the need to appear objective. Whether objectivity involves accuracy is a secondary concern.

Governments face this problem regularly. To avoid accusations of political influence they engage an army of external consultants to provide trivial advice that can easily be determined by internal staff. This army is the Shadow Public Service.

Oddly, critics fail to note that external advice that does not support a government position will be filtered anyway. Like a barrister in a criminal trial, they won’t ask questions they don’t already know the answer to.

I regularly deal with private economics consulting firms and can’t help but wonder how big an industry is supported by the farcical drive for an illusion of objectivity by government. I have personally engaged millions of dollars of work from private economics consulting firms for the sole purpose of having a basis for a predetermined decision that appears independent.

The final irony of it all is that the best qualified people tend to leave government departments to take on the same role as a consultant, but at five times the cost. And, of course, governments have a habit of filling vacant positions whether they are required or not. Either recruit the staff you need to provide proper advice, or get rid of them and draw upon the resources sitting in private firms. Don't waste money on a shadow public service unless they provide a real contribution beyond the objectivity illusion.

Monday, August 16, 2010

Competition Series Part III: History

Often forgotten in the competition debate are the reasons for a monopoly’s existence in the first place? A few are:

1. Mergers and economies of scale of private enterprise

2. Government development for its own needs (including defence)

3. Government intervention due to natural monopoly features (either too high risk for private enterprise or too much scope for price gouging)

4. Government intervention due to positive externalities (for example, cleanliness and health benefits of sewerage)

5. Government intervention due to fairness and equitable access – once a technology becomes a necessity it is politically expedient to promote fair access (including regional development)

While many may disagree that government involvement in some infrastructure networks was necessary from the start, citing the textbook benefits of the profit maximising natural monopolist, the onus should be on those promoting change to demonstrate that the world has changed sufficiently for competition and/or private firms to now deliver these services.

Historically, with the advent of new technology, government will typically step in if it sees benefits to centralisation - creating an entity tasked with equitable provision of the new service. Prior to centralised water and sewerage in cities, each property owner would have had a rainwater tank, bore or well to supply water, and a thunderbox for waste. Health benefits of newly designed reticulated sewerage systems were overwhelming (although it took some time before waste was treated in any fashion before being dumped into waterways). Private investment in sewerage reticulation could only recover cost from those who accessed the system, yet the social benefits were much broader. A government established (and subsidised) monopoly was the only way to go. A similar story can be told for water reticulation.

1. Mergers and economies of scale of private enterprise

2. Government development for its own needs (including defence)

3. Government intervention due to natural monopoly features (either too high risk for private enterprise or too much scope for price gouging)

4. Government intervention due to positive externalities (for example, cleanliness and health benefits of sewerage)

5. Government intervention due to fairness and equitable access – once a technology becomes a necessity it is politically expedient to promote fair access (including regional development)

While many may disagree that government involvement in some infrastructure networks was necessary from the start, citing the textbook benefits of the profit maximising natural monopolist, the onus should be on those promoting change to demonstrate that the world has changed sufficiently for competition and/or private firms to now deliver these services.

Historically, with the advent of new technology, government will typically step in if it sees benefits to centralisation - creating an entity tasked with equitable provision of the new service. Prior to centralised water and sewerage in cities, each property owner would have had a rainwater tank, bore or well to supply water, and a thunderbox for waste. Health benefits of newly designed reticulated sewerage systems were overwhelming (although it took some time before waste was treated in any fashion before being dumped into waterways). Private investment in sewerage reticulation could only recover cost from those who accessed the system, yet the social benefits were much broader. A government established (and subsidised) monopoly was the only way to go. A similar story can be told for water reticulation.

Thursday, August 12, 2010

Last piece of the population puzzle

I was pleasantly surprised by Dick Smith’s Population Puzzle documentary last night. He covered most of the key economic arguments against growth, including a rebuttal of the skills shortage and age dependency arguments. I was not taken by the food security argument, but was impressed by the way he highlighted the clash over land use on the urban fringes (where some of the most fertile soils are found).

Most importantly Dick raised the issue of vested interests promoting population growth early in his piece. He rightly singled out the property development lobby as a key exponent of higher population growth, and their obvious vested interests which do not align with the interests of most Australians.

Page 58 of today’s Financial Review has run a pro-population growth response to the Dick Smith documentary, advocating population growth on the grounds of economies of scale – an argument that is easily debunked.

A second argument appeals to economies of scale and suggests that with greater domestic consumption industries can expand to a point where they have economies of scale that make them internationally competitive. Why domestic population is currently a barrier to industry development is beyond me. If there are no artificial constraints on trade, shouldn’t the world be the marketplace of any industry even in its infancy? This argument only works if you couple high population with protectionism.

Economies of scale from increasing the size of the market only apply to monopolies in any case, and even then it is hard to know whether futher efficiency gains are possible (and whether they would be passed on to consumers).

But the confusion of the pro-population growth position is revealed later in the article when it states:

Of course it is possible to have economic growth without population growth – by setting up the conditions for higher productivity growth.

But the ‘meeting the challenges of growth’ argument persists in the end. We are apparently better off investing in massive duplication of infrastructure (roads, housing, energy and water) to accommodate higher population growth, which decreases productivity and economic growth, rather than focus on improving the productivity of the existing population - an absurd conclusion.

I have explained in detail in a previous post how housing investment and other infrastructure duplication does not improve productivity – it is a short term cost that simply allows more people to be equally as productive as the current population at some time in the future. Slower population growth is the recipe for improved per capita well being.

The relationship between growth and productivity is interlinked, but not in the way pro-population growth advocates maintain. Higher population growth is strongly negatively correlated with improved productivity. The graph below uses the ABS multifactor productivity measure and percentage change in population growth to demonstrate. Productivity improved most dramatically when population growth was around 1%.

The investment duplication argument is the final piece to the population puzzle.

The investment duplication argument is the final piece to the population puzzle.

Most importantly Dick raised the issue of vested interests promoting population growth early in his piece. He rightly singled out the property development lobby as a key exponent of higher population growth, and their obvious vested interests which do not align with the interests of most Australians.

Page 58 of today’s Financial Review has run a pro-population growth response to the Dick Smith documentary, advocating population growth on the grounds of economies of scale – an argument that is easily debunked.

A second argument appeals to economies of scale and suggests that with greater domestic consumption industries can expand to a point where they have economies of scale that make them internationally competitive. Why domestic population is currently a barrier to industry development is beyond me. If there are no artificial constraints on trade, shouldn’t the world be the marketplace of any industry even in its infancy? This argument only works if you couple high population with protectionism.

Economies of scale from increasing the size of the market only apply to monopolies in any case, and even then it is hard to know whether futher efficiency gains are possible (and whether they would be passed on to consumers).

But the confusion of the pro-population growth position is revealed later in the article when it states:

Of course it is possible to have economic growth without population growth – by setting up the conditions for higher productivity growth.

But the ‘meeting the challenges of growth’ argument persists in the end. We are apparently better off investing in massive duplication of infrastructure (roads, housing, energy and water) to accommodate higher population growth, which decreases productivity and economic growth, rather than focus on improving the productivity of the existing population - an absurd conclusion.

I have explained in detail in a previous post how housing investment and other infrastructure duplication does not improve productivity – it is a short term cost that simply allows more people to be equally as productive as the current population at some time in the future. Slower population growth is the recipe for improved per capita well being.

The relationship between growth and productivity is interlinked, but not in the way pro-population growth advocates maintain. Higher population growth is strongly negatively correlated with improved productivity. The graph below uses the ABS multifactor productivity measure and percentage change in population growth to demonstrate. Productivity improved most dramatically when population growth was around 1%.

Wednesday, August 11, 2010

Very interesting links

Following my previous post on the Debt Reduction Taskforce, I thought I would provide some links that explain my views on monetary theory more explicitly. Essentially, the money multiplier is a myth, and money is created first by debt, and reserves are accumulated after the fact if necessary - try Bill Mitchell’s blog for an explanation of Modern Monetary Theory (which is close to my personal views), and this site for more detailed discussion on the multiplier myth.

Ross Gittins reiterates my population growth arguments

Environmental concern and unemployment – a negative correlation. We are all too happy to worry ourselves about the environment when the going is good, but in a recession we suddenly shuffle the environment down our list of concerns.

Update on skills shortage and emigration of Australian trained professionals. This recent research suggests that “positive selectivity is stronger where the reward to skill in the destination is relatively large”. Translation: those who pay get the skills they desire.

Economists applying statistical techniques to strange social phenomena - worship and sacrifice:

The theory we test is that, when faced with uncertainty, individuals attempt to engage in a reciprocal contract with the source of uncertainty by sacrificing towards it. In our experiments, we create the situation whereby individuals face an uncertain economic payback due to “Theoi” and we allow participants to sacrifice towards this entity. Aggregate sacrifices amongst participants are over 30% of all takings, increase with the level of humanistic labelling of Theoi and decrease when participants share information or when the level of uncertainty is lower. The findings imply that under circumstances of high uncertainty people are willing to sacrifice large portions of their income even when this has no discernable effect on outcomes.

The Superstar Effect – when you receive massive gains from being marginally better than second best. The paper is here. I read once that the Beatles were probably underpaid for the wellbeing they imparted on the masses through their music. My view was that they earned a pretty penny. They were probably only a little better than the next band that would have formed and become an international sensation had the Beatles never existed. In the purest economic sense they were superstars.

Ross Gittins reiterates my population growth arguments

Environmental concern and unemployment – a negative correlation. We are all too happy to worry ourselves about the environment when the going is good, but in a recession we suddenly shuffle the environment down our list of concerns.

Update on skills shortage and emigration of Australian trained professionals. This recent research suggests that “positive selectivity is stronger where the reward to skill in the destination is relatively large”. Translation: those who pay get the skills they desire.

Economists applying statistical techniques to strange social phenomena - worship and sacrifice:

The theory we test is that, when faced with uncertainty, individuals attempt to engage in a reciprocal contract with the source of uncertainty by sacrificing towards it. In our experiments, we create the situation whereby individuals face an uncertain economic payback due to “Theoi” and we allow participants to sacrifice towards this entity. Aggregate sacrifices amongst participants are over 30% of all takings, increase with the level of humanistic labelling of Theoi and decrease when participants share information or when the level of uncertainty is lower. The findings imply that under circumstances of high uncertainty people are willing to sacrifice large portions of their income even when this has no discernable effect on outcomes.

The Superstar Effect – when you receive massive gains from being marginally better than second best. The paper is here. I read once that the Beatles were probably underpaid for the wellbeing they imparted on the masses through their music. My view was that they earned a pretty penny. They were probably only a little better than the next band that would have formed and become an international sensation had the Beatles never existed. In the purest economic sense they were superstars.

Tuesday, August 10, 2010

Population problem? It’s called longevity

Population growth advocates often rely on the ‘age dependency ratio’ as their core economic argument. This ratio is the population aged over 65 divided by the population aged 15-64. To give this measure meaning there is an assumption that people will not work beyond age 65 and will therefore be need to be financially supported by those at a working age. Workers will get less of the return on their productive output because it needs to be shared with more non-workers. Essentially, the percentage of people in the formal economy will decline.

I have a different opinion on the age dependency ratio. I see it as a shining beacon of success. People are working for shorter periods of their life. We as a group are finally taking some of our productivity gains of the past half-century in the form of leisure time.

Whether or not you agree this a problem, the suggested solution of population growth is, in reality, counterproductive, and will only aggravate the situation. An increase in the dependency ratio is principally caused by improving longevity. If each generation lives longer than the last we will face this problem even with a growing population. Simply adding more at the bottom of the population pyramid to keep it bigger than the top has the apt label ‘population Ponzi scheme’. Indeed, to counteract this trend would require a significant increase in the natural birth rate, or age biased migration policies, or even the extreme scenario of sending migrants back home when they hit 65. None of these are desirable.

Sunday, August 8, 2010

Debt reduction taskforce - bad timing

Tony Abbott recently announced his plan to establish a debt reduction taskforce to reduce government debt that he believes Labor foolishly incurred. I have no problem with governments paying down debt and aiming to have a zero debt balance over the business cycle, but does he really think that governments should pay down debt while the citizenry is trying to do the same? To me this sounds like a recipe for disaster.

Debt deflation is what happens when indebted households and businesses start to pay off debt after a period of debt accumulation. Money used to pay debts is not used for consumption and no longer circulates in the economy. This decreases demand, but also reduces the money supply. The net effect is to slow economic activity and reduce prices (deflation). To read quality analysis of debt deflation read Steve Keen’s superb articles here.

The government response to this should be to print money. Because a portion of the new money is used to pay debts, a far smaller portion circulates in the economy to cause inflation. If it is done well, it should slow deflation, keeping demand and prices stable, and allow debts to slowly be repaid without the value of debt rising in proportion to incomes. Whether this will promote further malinvestment (investing in non-productivity improving assets) remains to be seen.

Establishing a taskforce is a clear sign that it is not Abbott’s intention to pay down government debts by printing money. His plan appears to be the reduce government spending to pay debts – the exact same thing households are currently doing.

This will only exacerbate the decline in demand and accelerate our march towards deflation.

Debt deflation is what happens when indebted households and businesses start to pay off debt after a period of debt accumulation. Money used to pay debts is not used for consumption and no longer circulates in the economy. This decreases demand, but also reduces the money supply. The net effect is to slow economic activity and reduce prices (deflation). To read quality analysis of debt deflation read Steve Keen’s superb articles here.

The government response to this should be to print money. Because a portion of the new money is used to pay debts, a far smaller portion circulates in the economy to cause inflation. If it is done well, it should slow deflation, keeping demand and prices stable, and allow debts to slowly be repaid without the value of debt rising in proportion to incomes. Whether this will promote further malinvestment (investing in non-productivity improving assets) remains to be seen.

Establishing a taskforce is a clear sign that it is not Abbott’s intention to pay down government debts by printing money. His plan appears to be the reduce government spending to pay debts – the exact same thing households are currently doing.

This will only exacerbate the decline in demand and accelerate our march towards deflation.

Competition Series Part II: Theories, assumptions

Let us look at the theory to see why the productivity gains from Australia’s pursuit of competition reform have been so hard to come by. Oliver Williamson’s 1968 model of the competition-coordination tradeoff is a good starting point.

The assumptions in Williamson’s model are that the monopoly industry has a lower marginal cost than competitive firms, that the monopolist sets their profit maximising price according to traditional economic theory, and that in a competitive market firms set their prices at marginal cost.

The graph below shows the resulting welfare implications of this model.

In this situation, while the competitive firms face higher costs (MC2), they set a price lower than the profit maximising monopolist (at P2 instead of P1). The welfare implication is that the area A is transferred from producer to consumer surplus, area B is the loss of producer surplus due to coordination costs, and area C is the gain to consumer surplus. There is a net loss of social surpluses (including all producer surplus) from competition in this model, however there are significant gains to the consumer surplus (areas A and C).

In this situation, while the competitive firms face higher costs (MC2), they set a price lower than the profit maximising monopolist (at P2 instead of P1). The welfare implication is that the area A is transferred from producer to consumer surplus, area B is the loss of producer surplus due to coordination costs, and area C is the gain to consumer surplus. There is a net loss of social surpluses (including all producer surplus) from competition in this model, however there are significant gains to the consumer surplus (areas A and C).

For a net gain to consumers in this model, two conditions need to be met:

1. The profit maximising price of the monopolist is higher that the marginal cost to the competitive producer (MC2 < P1), and

2. The competitive producers set prices at marginal cost (P2=MC2)

Unfortunately, neither of these conditions can be known in advance. In fact, if we drop just the second assumption, which has been proven many times to be far from realistic, the chances of a competitive market generating greater surpluses than a profit seeking monopolist greatly diminishes. In the above diagram this would mean that P2 is somewhere above MC2 (and of course we still don’t know if MC2 is below P1).

The assumptions in Williamson’s model are that the monopoly industry has a lower marginal cost than competitive firms, that the monopolist sets their profit maximising price according to traditional economic theory, and that in a competitive market firms set their prices at marginal cost.

The graph below shows the resulting welfare implications of this model.

For a net gain to consumers in this model, two conditions need to be met:

1. The profit maximising price of the monopolist is higher that the marginal cost to the competitive producer (MC2 < P1), and

2. The competitive producers set prices at marginal cost (P2=MC2)

Unfortunately, neither of these conditions can be known in advance. In fact, if we drop just the second assumption, which has been proven many times to be far from realistic, the chances of a competitive market generating greater surpluses than a profit seeking monopolist greatly diminishes. In the above diagram this would mean that P2 is somewhere above MC2 (and of course we still don’t know if MC2 is below P1).

Thursday, August 5, 2010

Scared of deflation?

I have always been puzzled at the assymmetry of 'flation fear'. A little inflation is good, but a little deflation is a scary thing.

Paul Krugman outlines the general argument as follows:

So the argument that deflation is a bad thing is also an argument saying that some economic problems get worse as inflation falls, and that too low an inflation rate may actually be economically damaging.

For the life of me I can't see how an inflation rate of zero can be damaging in the long run. Also, if we look at Krugman's argument in reverse, more inflation is better. Why isn't the optimal inflation rate zero instead of some positive number? Why 3% instead of 10%? Do human have an inbuilt behavioural trait that only we are able to plan and invest knowing that currency in the future will worth less rather than more?

Steve Landsburg on the other hand makes the argument that deflation fears are not justified by economic theory or evidence - I don’t see the problem in theory and I don’t see the problem in practice.

And he concludes that even if deflation is bad, it is easily solved.

Even if deflation is a bad thing, we know how to solve it. Print enough new money and people will eventually start spending it. It’s alleged that no matter how much you print, it can all just fall into the liquidity trap, and it’s alleged that this is what happened in Japan over the past decade. But I am sure the Japanese just didn’t try hard enough. Liquidity trap or not, I guarantee you there’s a central banker in Zimbabwe who knows how to fight deflation. If we really get into trouble, all we have to do is hire him.

As I have noted before, the world survived just fine for a long period of time with inflation at zero on average. Positive inflation in the long run did not occur until post WWII. Some might even argue that this is simply the longest ever business cycle stimulated by enough debt to keep inflation positive, and that the next fifty years, subject to international politics, might see prolonged deflation.

Avoiding deflation in the short run may have made the global economy far less stable in the long, long run.

Avoiding deflation in the short run may have made the global economy far less stable in the long, long run.