My first ever public comment about COVID was this. I was both prescient and wrong.

Everyone has lost their shit about coronavirus as if lives lost this way are worth orders of magnitude more than lives lost any other way. In two to three weeks time the reality will set in that there are real costs of locking down society that can be measured both in value of resources wasted and in blood. All perspective has been lost at present.

If only I’d written years instead of weeks, then it would have been spot on.

As someone who has thought about health policy, well-being, and trade-offs for many years, my first reaction to the media coverage of COVID and the mystery China virus was to ask the following question: What is the normal number of deaths in a city the size of Wuhan? Without this context, all the media coverage made no sense. A city with 12 million people can expect about 96,000 deaths a year. That’s 264 a day.

So when I read headlines like “Death toll rises to 600” and that smoke from crematoriums working overtime was filling the city, I had a reasonable baseline from which to sniff out nonsense. The numbers mattered then and they still matter now.

If you search online for news articles of COVID or coronavirus deaths from February 2020 you will see just how small the death numbers are and how crazed and fearful the reporting was. Some of the reporting just had made-up figures, with orders of magnitude differences from one article to the next. No one really cared.

Even at this early stage, the lack of deadliness of the virus was becoming clear for those who wanted to find out. The case fatality rate was likely to be sub 0.7%, even with relatively limited testing (i.e. 0.7% of known cases, not all cases). Clearly, this implied that early estimates were hugely biased because infections were far more widespread than initially assumed.

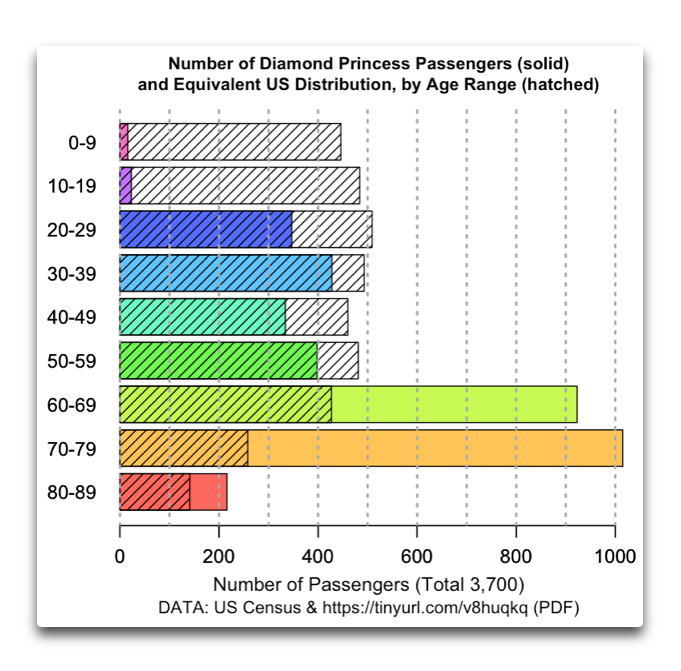

The Diamond Princess cruise ship had 3,711 people on board and had 14 deaths. On this cruise, 0.37% of people died over a two month period. Is that good or bad?

We know that background mortality is about 0.8%. So every two months you can expect 0.13% of people to die. But this is across the whole age distribution. Even a small skew towards the elderly massively increases this number. For example, in your 80s you have a one in twenty chance of dying each year on average. In your 90s, a one in five chance.

The age distribution of the Diamond Princess was super high, so 0.37% of people dying within two months is totally within the normal range.

We already knew then from the Italian outbreak that the average age of COVID deaths was higher than deaths from all other causes combined.

Taking all this information together was pretty encouraging. This is why herd immunity was thought to be simply a matter of months away. Flatten the curve for two weeks, then a month or two later the whole thing would be over. No one expected to be having masks, border closures, vaccine mandates and passports for two years.

Of course, none were taken up. But looking back, they were much more sensible than what we got with a JobKeeper giveaway, a Cashflow Boost, that cost hundreds of millions and resulted in a net upwards redistribution of wealth.

Read the rest of this post at my new substack page and please subscribe there to get new posts to your email.

*This article is based on a submission to the Housing Supply Inquiry that I contributed to for Prosper Australia.

This neglected economic puzzle has become a heated policy debate. Rapidly rising dwelling prices globally have grabbed the attention of policy makers. Many have subsequently targeted planning and zoning as areas for housing reform. Australia, New Zealand, the United Kingdom and various states in the United States, are conducting new reviews into planning, housing supply, and prices.

Unfortunately, most analysis of housing supply conflates density (dwellings per unit of land) and the rate of new housing supply (new dwellings per period of time across all sites). This is because the time dimension of the investment decision facing a landowner is typically ignored in the economic analysis of housing supply.

But the optimal inter-temporal choice of landowners is hugely important for understanding the rate of new housing investment in property markets. Just as there is an optimal density of development that maximises the value of the site, there is also an optimal rate of sales of new dwellings per period that maximises the value of the site.

Across all candidate development sites in a region, the rate of new housing development (new dwellings per period of time) is known as the market absorption rate or build-out rate. Regardless of planning or zoning, this rate is the result of many landowners making individually-optimal choices about when and how fast to develop.

The economic logic behind the market absorption rate is described in Murray (2021). Some key elements of it are important to clarify. Owners of the property where a new home can be built already possess an asset on their balance sheet worth exactly the market value of the land. Developing that land with a new dwelling is a balance sheet reallocation. If developed for immediate sale, the property owner is swapping an undeveloped site asset for a cash asset. If developed for rental, the owner has swapped an undeveloped land and cash asset (to fund construction) for a dwelling asset.

Whether these asset swaps are economically viable depends on the relative returns to each. Only in a market where demand is rising does it make sense to increase the rate at which undeveloped land assets are swapped for cash assets. When market demand is falling and very “thin” (few buyers at current prices), it makes sense to slow the rate of new housing development. Other factors like interest rates (the return on cash after sale), taxes on land ownership (that reduce the return to retaining ownership of undeveloped land), and the ability to vary the density of development in the future (a flexible planning system can make delay more profitable by allowing higher density in the future, increase the return to delay), all have effects on this rate.

One interesting problem for this new type of analysis is demonstrating how economically important the payoff to delaying new housing development is for property owners. To address this, I am proposing here some new metrics that can be applied to housing developments to demonstrate the degree to which varying the rate of sales in response to market conditions increases the total economic returns from developing a site. These metrics demonstrate that independent of any planning controls on density, there is a “speed limit” on the supply of new housing in the form of the market absorption rate.

Development Rate Ratio (DRR)

How fast did the subdivision develop compared to how fast it could have if the maximum observed rate of sales was sustained?

Housing developers often argue that new housing is being built as fast as the planning system allows. Indeed, quite a deal of economic analysis also makes this assumption. However, once a subdivision or apartment building is approved by the planning system, the private choices of the developer determine how fast the approved new housing is developed. This includes how fast they sell, which is the key limiting factor of the build-to-order model of new housing production.

To demonstrate the degree to which these private choices limit the potential rate of new housing supply I proposed looking at the Development Rate Ratio (DRR).

The DRR shows the average speed of development as a ratio of the maximum speed, using the average monthly rate in the fastest three-month window. A lower number indicates that the new housing development proceeded more slowly than was demonstrated to be possible.

Development Rate Variability (DRV)

A second metric is Development Rate Variability (DRV). DRV is the ratio of the fastest speed of monthly sales to the slowest monthly sales during a development. This shows how sensitive to market conditions the choice of sales can be. A higher DRV shows how much the private choices of housing developers change the rate of new housing supply.

It may be argued that it is impossible to sell fast in a depressed market. But this is only true if prices are held constant. The very heart of the housing supply debate is whether planning changes create conditions for private housing developers to build faster at lower prices.

These two new metrics can help paint a picture of the variation in the market absorption rate due to the private choices of landowners. To complement these metrics, we also create new metrics of the economic returns available in housing development from varying the rate of supply in response to market conditions.

Delay Premium (DP)

What is the economic gain from varying the rate of supply of new housing to “meet the market”?

To answer this question a sensible counterfactual must be established. The counterfactual implied in most economic analyses of housing is that housing is supplied once the market price gets above the feasible price for development. In other words, housing developers fix the price of all housing (or land lots) at the beginning of the project (a fixed point in time) then vary only the speed of sales to match market demand at that initial feasible price.

The dynamic approach recognises an economic return to varying both the rate of supply and the price. This is then the difference in revenue between the following two approaches.

Setting a price at the beginning of the project and selling all dwellings or housing lots at that price until the project is completed

Varying both the rate of supply and price to maximise profits from the project.

A metric that identifies the economic gains to delay is the Delay Premium (DP). The DP is the share of total revenue that was made by varying price as well as quantity (ignoring discounting) and is calculated as follows.

Two parts of this equation need some explanation. First, when applied to detached housing subdivisions the total revenue is for land only, not for homes. This is because the additional gain from building the home comes with added construction costs leaving the land value as the net income. Second, the reason for including the minimum land price rather than the initial price is because the lowest price in the sequence of sales indicates the minimum willingness to sell.

A higher DP means that a larger share of the total revenue came from actively varying both price and quantity during the selling period.

Available Delay Premium (ADP)

Another metric that shows the economic gains to delay is the Available Delay Premium (ADP). It measures the maximum difference in sales price over the life of a project (the peak price per sqm that often occurs at the end of a project and the lowest sale price that usually occurs near at the beginning) multiplied by the total sold land area as a proportion of actual revenue. This metric indicates a theoretical maximum degree to which revenue could have varied (as a proportion of actual revenue) if all sales were made at the highest price compared to all sales being made at the lowest price.

The interpretation of the ADP is to show how important choosing the timing of sales can be to the final returns of a project. A higher ADP indicates that varying sales rates due to changes in demand, and hence price, will have a higher economic payoff.

Applying these metrics

Jordan Springs is a 900-hectare residential subdivision located in Penrith (53km west of Sydney’s CBD) and was approved for development in 2009 with the first residents moving in during 2011.

By 2012 the development was owned by Lendlease, which published in its annual report that year that the area would ultimately provide over 2,000 detached dwellings and 200 apartment dwellings, with an expected 10-year development timeline. The subdivision masterplan is below.

Unfortunately, data on land and house sales in this subdivision is only available to me at the moment from 1st October 2015 to 8th October 2021, a period over which there were an estimated 2,131 new land lot or dwelling sales.

Summary of absorption rate metrics

The four absorption rate metrics for the available data on this large subdivision project are summarised in the table below.

In this data, total revenue was around $1 billion. The 0.13 DP represents about $137 million of value that was gained by varying prices during the project rather than setting the minimum profitable price and selling all lots at that price. The difference in revenue between selling all lots at the lowest per square metre price and the highest price was $310 million. These figures also provide insight into the variability and risk involved in land and housing development.

Further analysis and detail

It is also worth looking at the variation in sales and prices over the available data for the Jordan Springs project.

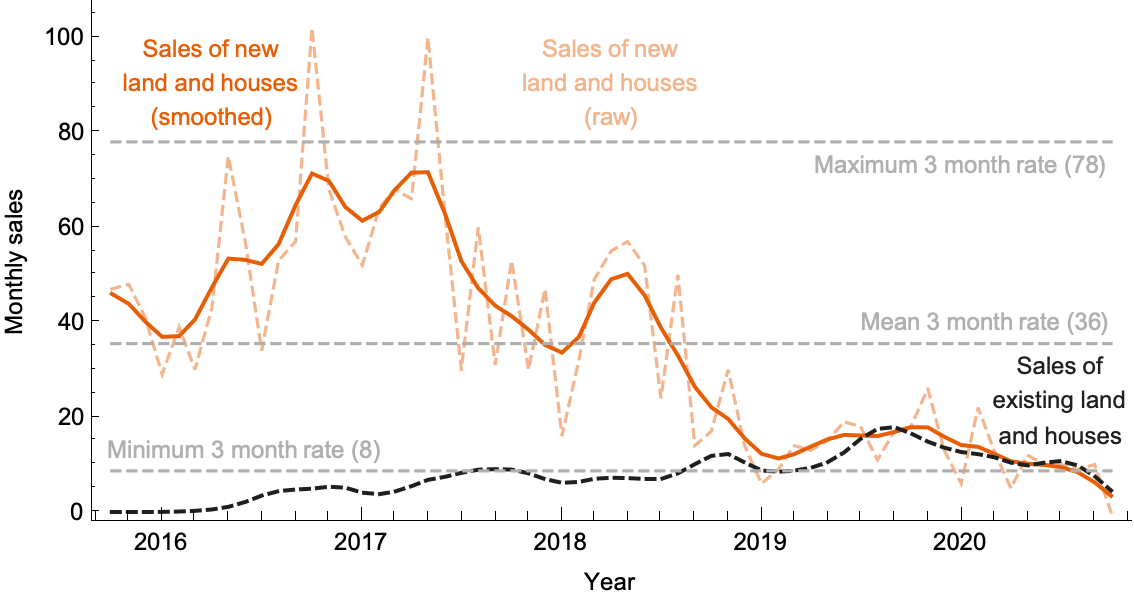

The chart below shows the smoothed monthly rate of land and house sales for new dwellings (orange), alongside the repeat sales (dashed black) over time. Minimum, maximum and mean sales rates are marked (which are used to generate the DRR and DRV metrics). Notice that in the quiet housing market of 2019 that sales were much slower than in the busy 2016-17 market period.

The next chart below shows the land price per square metre observed in the sales data over the same time period, with maximum, minimum and mean prices market (which inform the DP and ADP metrics). During this five year window, land prices varied by around 30% (the ADP metric) but had noticeable peaks and troughs that coincided with macroeconomic conditions.

Finally, we can look at the relationship between price growth and the rate of supply in the final chart below. Although these data points do not generate a statistically significant relationship, visual inspection shows clearly that periods observing price growth also saw faster new supply, especially in earlier development stages during 2016-18, as expected if the developer is optimising sales rates and price to maximise their revenue (as predicted by the logic of the market absorption rate).

The enormous variation in the rate of supply in large projects such as Jordan Springs, with thousands of approved dwellings, is a clear indication of macroeconomic and market conditions being the main determinant of the rate of new housing supply.

I listened to a frustrating Sam Harris podcast about COVID policy yesterday. What struck me about these "expert" commentators was that they

kept finding reasons to link COVID policy back to Trump, which was weird, and

all but ignored the enormous age variation in COVID risk.

Both these seem like popular ways of thinking, unfortunately.

I want to comment briefly on the second issue. This should help explain why I support vaccinations for the elderly but feel strongly against vaccinating children, vaccine targets and mandates.

The risk of serious illness or death with COVID is far more age-skewed than most viruses. In the below figure I show this skew. COVID is a serious disease for the elderly.

I also plot vaccine risks in the dashed orange. You might not be able to see it because it is so close to the axis. For age 70, the benefit-to-cost ratio of the vaccine is about 250x (i.e. the blue line is 250 times higher than the dashed orange line). A great outcome and something anyone would be foolish not to recommend.

But exponential curves are deceiving. Let's zoom in on this curve for young age cohorts. I do this below (curve equation is 10^(-3.27 + 0.0524xage)). Notice now that we are way down near the vaccine risk. It's close. I show a broad range of risks and call this COVID curve the risk of serious illness. I do this because reality doesn't follow the neat equation I used to plot the curve and children are likely even lower risk than shown.

In short, because the age skew of COVID risk is so severe, these huge many-hundred-times benefit-to-cost ratios can reverse at low ages so that the costs are many times the benefits. This is why so many doctors are calling for a halt to mandates for vaccinating children.

We should let this well-known information about COVID guide us rather than politics and panic.

Not that long ago Germany as a whole featured heavily in this debate over planning rules and house prices. With Frankfurt topping the latest UBS real estate bubble index, and Munich at number four, we don’t hear much about that anymore.

Tokyo is another city where planning rules are argued to have led to cheap housing.

Have we all forgotten that Tokyo was the world’s most expensive city not that long ago and is famous for how small its dwellings are? It also has less than 50% homeownership.

Across the central 23 wards of Tokyo, there are only 19sqm of dwelling space per person. Only 22% of Tokyo households have more than 29sqm of space per person. Across the prefecture as a whole, there are about 30sqm per person of residential space.

Australia has about 90sqm of internal residential space per person—roughly three times as much as Tokyo. Australia would need to nearly triple its population without building a single extra dwelling to have the same "housing abundance" as greater Tokyo, and would still have way more private garden space.[1]

Yes, there is an overall trend in Japan towards more dwelling space per person. But this is driven mostly by the rise in elderly households, especially elderly singles. When an elderly couple remains in their home after their children leave they increase the floor space per person even if that young adult child moves to an apartment with less space than their share of space at their parent’s home. When one person from an elderly couple dies, they leave behind an elderly single-person household, boosting the floor space per person metric. Many countries whose ageing populations are not as advanced as Japan’s will also see this same trend automatically.

Another issue is Japan’s long period of deflation. CPI is up 10% in Japan in the past three decades, while it’s up 300% in the US, for example. Average wages have also been flat for decades. It is not a good idea to compare rents or prices in Japan without factoring in their unique wage and consumer price conditions.

Overall I’m not persuaded that a housing market more like Tokyo’s is desirable. On the more substantial point that relaxing town planning rules got that outcome, I find little evidence.

fn [1] I’m wary of charts like the one below since the only statistics I know about dwelling sizes rely on self-reported estimates by various ad hoc surveys by statistical agencies.

“When I use a word,” Humpty Dumpty said in rather a scornful tone, “it means just what I choose it to mean — neither more nor less.” ’The question is,” said Alice, “whether you can make words mean so many different things.” ― Lewis Carroll, Through the Looking Glass

An increasing academic and policy focus on housing supply has unfortunately not brought with it an increase in clarity over the meaning of words. Words like housing supply, demand, zoning, price and affordability, have come to mean whatever the authors want them to mean.

This is unhelpful.

I've put together in the below table various potential meanings of these catch-all economic terms, and the words I think we should use instead to increase clarity.

For example, economists should be crystal clear that the economic price of housing is the market rental price (i.e. the price that measures the amount of good and services given up to get that good). The sale price of a dwelling is merely the market’s judgement of the asset value of buying a rental income stream in perpetuity and is heavily affected by prevailing interest rates (capitalisation rates), land and property taxes, and expectations of changes to the asset value (capital gains expectations).

With such a variety of definitions, what can the phrase “an increase in the supply of dwellings relative to demand will reduce dwelling prices” actually mean?

The obvious and strictly true definition is when the terms mean

supply → market willingness to sell housing in this period, demand → market willingness to pay for housing in this period, and price → the sale price of a dwelling in this period.

This merely describes asset market bid and offer schedules. When there is a "supply shift" in these schedules that massively reduces prices, we call that a market crash (a topic that is also poorly understood). But the economics of housing stock change is more sophisticated than this.

Supply and demand might also mean number of dwellings and total population—completely different ideas from bid and offer schedules in asset markets, instead focussed on material quantities that are expected to move together.

Sometimes supply is used to mean zoned capacity (how much can build built within current zoning rules) and is often assumed to be synonymous with the absorption rate (how quickly the market will develop new housing subject to asset market conditions). Changing zoned capacity does not necessary change the absorption rate, yet they are often described as one and the same thing.

Perhaps if we could describe what we mean more specifically we can start to allow the evidence to support or disprove theories about how the housing and property market operate.

I'm open to improving and expanding the table with better, or more widely used, terminology and will update and refine it over time.

A video of my testimony to the inquiry is here (from 11:00:00)

My full written submission is here and my follow-up response to questions raised is here.

_____________

I believe I am one of the few witnesses who has worked for residential and industrial property developers, in government departments dealing with infrastructure charges and regulation, and now as a housing researcher.

To be clear, Australia has more, bigger, better dwellings per capita than any point in history. We are also building new dwellings at a near record pace in a period where population growth is the lowest in decades.

More housing is better than less housing. Absolutely. I agree.

The argument I disagree with is that private landowners want to build faster, but only pesky council and state government red tape is slowing things down.

While I certainly have many ideas for improving and simplifying the planning system I see this as a separate topic to housing affordability.

We’ve heard from previous witnesses that housing developers have a lot of trouble building on unzoned land. No doubt. The whole point of unzoned land is to not have development at that location and get it located in the zoned land. It’s hardly evidence of anything except that these developers are bad at their jobs, always buying the wrong land for what they want to build.

Indeed, they certainly appear to be terrible lobbyists. If what they claim is true about zoning keeping prices up, then lobbying for mass rezoning is financial suicide. It would vastly increase the number of competitors in their market and reduce prices, wiping billions in value from their balance sheets. What sort of industry lobbies for that?

Perhaps this story is a lie.

In 2003, the AFR ran the headline “Brisbane running out of land for housing”, with land for housing expected to run out by 2015 according to the same expert lobbyists who have attended this inquiry. Yet detached housing lot production was 30% higher in the 6 years since 2015 than in the 6 years prior.

Are they terrible at their jobs? Or just telling stories that conceal the true nature of property markets?

Remember, only landowners can choose to make planning applications. Only landowners can choose when to build homes. Councils don’t do this. There is no speed limit to building new housing in the planning system. Planning regulates the location of different uses and densities, like road lanes regulate locations on the road. Density (dwellings per unit of land) and supply (new dwellings per period of time) are completely different concepts. More density does not equal faster supply.

The key issue at stake in this debate is that land is an asset. It is therefore priced like one. This is why when it is a good time to buy it is also a good time not to sell.

This is true for developed and undeveloped land. Stocks of undeveloped land sit on the balance sheet of developers, earning a return by growing in value while undeveloped.

The trade-off between the return from delaying developing land, versus developing now, creates a built-in market speed limit on the rate at which private landowners develop. As a previous witness mentioned, “… if you are a property owner or developer that had land that was consented and you hadn’t sold it a year ago then you are in a very strong position.” Builders might like to build faster, but landowners prefer to maximise returns on their assets.

We can see how this pays off with a case study of Jordan Springs, a Lendlease subdivision of around 2,000 housing lots in Sydney that took a decade to sell. I looked at the sales rates over time and saw that the average rate was only 45% of the peak rate (3-month average), though some periods had sales just 12% of the peak rate. The speed of developing new housing lots was far below the capability of developers and the capacity of zoned land. By selling at this slower rate, and capturing overall market gains in the form of higher prices, they made an additional $137 million on the project. Prices were 31% higher at the end than the start for land lots on a per sqm basis.

It would have been financially irresponsible of them to develop faster than they did.

I’m not saying that this behaviour is wrong, or a conspiracy, or even that it has major price effects. The stock of housing only changes a couple of percent a year at the best and small changes to those small changes make tiny price differences. This is just normal market behaviour. This is why for the century prior to the existence of zoning we had the same issues of unequal access to land and housing ownership, only much worse.

The current housing asset price boom is a global one. Average prices are up 20% in the last year in the US, the same as Australia, and many places that were previously lauded as having flexible zoning, like Germany and cities in Texas, have had the highest price growth. What we are seeing is a period of global asset re-pricing, as intended by monetary policy.

If you really want more homes build them. Flood the market with a public housing developer—you know, just in case the private developers don’t do what they said they would. It might be a sensible insurance policy. No doubt the property lobbyists will find something wrong with this, even though it is exactly the outcome they pretend to be lobbying for—more competitors and lower prices.

A discussion about the best way to provide below-market-priced housing popped up on Twitter recently. Peter Tulip noted many of the limitations of such systems—queuing, quotas, qualifying criteria, etc—concluding that a cash payment to help pay market rents is an economically-efficient way to get the policy outcome of reducing housing costs to low-income households.

Many submissions to the Falinski inquiry call for “inclusive zoning”, “affordable housing”, “social housing” and similar programs. A central feature of these policies is rent control, with housing being allocated by a mix of queueing, bureaucratic formula and randomness. 1/6

I am not against providing such cash payments. They are clearly better than nothing. But the reason I believe governments should build and own some housing is that it provides a better bang for your housing subsidy buck.

Consider the two alternatives over a “tenant life” of say 30 years.

With cash rental assistance, the government pays, say for the sake of argument, $13,000 per year the first year. But to have a meaningful effect this must grow over time to reflect growth in rents and incomes. At a 2% growth rate, by year 30, the subsidy is $23,000 and over 30 years the total subsidy paid is $527,000. The present value of this 30-year flow of subsidy payments at a 2% discount rate is $374,000.

With public housing ownership, the government builds or buys a dwelling worth $500,000 today to supply that dwelling at a rent that is currently $13,000 below market rent per year (i.e. the same rental subsidy to the resident). The remaining rent paid by the tenant covers ongoing costs only. Like the cash rental subsidy, the gap grows over time to be $23,000 in the 30th year. Instead of $374,000 in present value terms, this option costs $500,000 today to build or buy the dwelling (much less if built on under-utilised publicly-owned land).

However, with public housing ownership, a government agency owns the property at the end of the 30 years. Over this period, the asset value grows. Even if it grows in line with the 2% growth of local incomes it means that the property is worth $890,000. In reality, because incomes at a location rise faster than the average (because cities expand), it is likely to be more. For reference, this is only a 76% rise in three decades; a conservative figure when compared to the 143% price rise seen in Australia’s capital cities in the past 18 years.

The table below shows a comparison of the two alternative ways of providing the same value of housing subsidy to a resident over 30 years. Although the public housing ownership option costs $500,000 upfront, today's value of the final sale price is $490,000, leaving a net economic cost of just $10,000. This approach gets 40x better value for the budgetary spend. If capital growth is closer to historical norms then public housing can more than pay for itself.

What we learn from this is that

The cost of rental assistance over the long term is not much different than simply buying a dwelling and giving it to the household ($374k vs $500k).

The cost of rental assistance over the long term is much more than providing the same rental subsidy via owning the property ($374k vs $10k)

Getting out of the housing ownership game over the past three decades and shifting towards rental subsidies has cost government budgets billions.

[UPDATE] I've updated the figures to reflect 2% growth of incomes and rents and 2% interest and made the spreadsheet available here. Play around with the numbers.

[UPDATE] People seem to think that interest payments need to be taken into account somewhere. They do not. Prevailing interest rates are incorporated via discounting.

[UPDATE] Thanks to Jago Dodson for letting me know that a 1993 review by the Industry Commission (now Productivity Commission) ranked public housing first in terms of efficiency and cost-effectiveness out of a variety of alternative housing subsidy approaches they assessed.

[UPDATE] Thanks to Vivienne Milligen for letting me know that the 1989 National Housing Policy Review found similarly—that public ownership of housing is the lowest-cost strategy for housing poverty relief.

Part of political theatre that comes with rising dwelling asset prices is to fake concern for the non-homeowners. In the past two decades, this has taken the form of blaming supply and town planning for the fact that investors arbitrage returns and leverage into housing when interest rates fall.

It is nonsense from top to bottom.

We know this because the most recent of many UK reviews into housing supply concluded that it was not desirable to implement any new incentives for housing developers to build faster if that meant they had to accept lower prices.

The Letwin review of housing build-out rates was weird.

After learning that private landowners don't voluntarily flood the market to depress prices, they then decide that any policy to change that would be bad.

We know this because a 2004 Australian review concluded that the stock of housing changes by such a small amount each year that even very large changes to the rate of new supply will have small price effects.

From way back in 2004 when the Productivity Commission looked at the evidence and concluded that higher rates of new housing supply can't change prices much. https://t.co/yAD7CZSNVQpic.twitter.com/qPtpuLC7K1

We know that it suits vested interests in the property market to focus the debate on non-solutions that provide them windfall gains in the form of rezoning.

Housing markets are quite easy to understand. The difficult part is first unlearning all the nonsense that fills the newscasts and journals.

Australia’s latest inquiry into housing supply has begun. I took the chance to make a submission outlining my views on the housing market and writing a document that I hope provides some lessons about how to understand housing.

There are more, bigger, better, dwellings per capita in Australia in 2021 compared to any point in history.

Multiple government inquiries at all levels over the past two decades have ostensibly sought to find the cause of house prices hidden in the pages of local zoning laws.

Dwellings are assets and are priced based on financial market conditions.

Density (dwellings per unit of land) and the rate of supply (new dwellings per period of time) are conceptually different but often confused in housing supply discussions.

This submission argues that market housing supply has exceeded household demand. State planning systems have flexibly accommodated new supply while regulating the location of different types of dwellings.

Compared to household incomes and rents, the cost of buying a home (measured by mortgage payments) in 2021 is historically cheap. This is due to lower interest rates and is why intercensal homeownership is expected to rise in 2021. However, asset price adjustments will mean that this situation will not persist.

Taxes on property are efficient and fair and do not add to housing costs but rather subtract from property values.

Affordable housing is cheap housing. Cheaper housing means lower rents and prices. Any “affordability” policy that reduces market prices will remove billions in landlord revenues each year, transferring that value to tenants, and trillions in housing asset values, with that value transferred to future buyers.

Fostering parallel non-market housing systems, just as public healthcare provides a non-market medical system, can be an effective way to improve housing affordability.

There are no local, international, or historical examples of planning reforms leading to cheaper housing. Indeed, a Productivity Commission review concluded “given the small size of net additions to housing in any year relative to the size of the stock, improvements to land release or planning approval procedures, while desirable, could not have greatly alleviated the price pressures of the past few years.” (p154)

The GAMSAT is an entrance test that all prospective students to medical schools in Australia must take.

I want to use a hypothetical scenario about this test to understand how it might be possible to determine whether it constrains the rate at which new doctors are trained.

The hypothetical

Some people say that this test affects the total stock of doctors and hence the price of medical services.

You have the following information and are asked whether this is a potentially important concern.

In addition, you know that

Only those with a bachelors degree are eligible to take the test.

The number of people graduating with bachelors degrees each year is nearly a consistent 20,000 per year, adding to a large pool of candidate test takers.

Those who do not pass the GAMSAT can re-sit the test as many times as they like in subsequent years.

Those who pass have the option, but no obligation, to attend medical school.

You must re-sit the test if you do not go on to medical school within three years.

100% of those that decide to attend medical school complete it and become practising doctors.

You are asked to advise whether the pass rate contains information about the degree to which the entrance test determines the stock of practising doctors. Some say the high pass rate and ability to re-sit the test shows that the GAMSAT test is not a constraint on the supply of doctors.

Let us think this through.

The system perspective

The first thing to do is get a good understanding of the system with the numbers involved. The below diagram shows how the stock of potential candidates flows through the testing system to become doctors. There are three decision points.

The choice to take the GAMSAT test

The pass/fail choice

The choice to proceed to study after a pass

I draw these choices as taps that control the flow of “water” into the “buckets” (stocks of people at each stage). Notice that two of the choices return the people back to the pool of candidates—the pass/fail, and the study/delay choices.

Quite clearly the most important choice in getting water from the stock of potentials to the stock of doctors is the choice to sit the GAMSAT test in the first place.

This choice has by far the biggest effect on the outcome, with its variability accounting for the variation of flows through the system by a magnitude of 16x. One year 50 people took the test. One year it was 800.

None of this variation appears due to the GAMSAT test as the pass rate is unchanged and the choice to proceed is unchanged (we will return to this assumption).

By looking at the system in this way we can see that the maximum amount of additional doctors getting through the process by removing the GAMSAT test is 6%. It is likely to be less than this because those who fail often repeat the test.

You conclude that the GAMSAT test is at most an extremely minor factor influencing the rate of supply of new doctors.

A new argument

However, some argue that there is no evidence in the 94% pass rate that the GAMSAT is not a major constraint.

The argument is that the existence of the test reduces the number of applicants. Those who are likely to fail will know in advance and choose not to take the test. Therefore, even if the pass rate was 100% the GAMSAT could still be a major restriction on the flow of new doctors. It might be a plausible assumption that the variation in the choice to sit the test is explained by the number of people who believe they will pass it.

So we have two potential mechanisms of actions of the GAMSAT test.

A direct effect due to the pass rate

An indirect effect due to reducing the number who choose to take the test

How could we tell if the second mechanism was important?

We could look further up the system and see if the variability of the choice to take the test is related to factors regarding the test stringency, or other factors. But how would you measure test stringency if not for the pass rate?

You would need a third variable that measures test stringency that is unrelated to the pass rate, and that correlates closely with the number of test-takers. Possible? I’m not sure.

The problem is that if the second indirect effect dominates, then what are we to make of variation in the pass rate? What if a 10% pass rate is the norm, and that falls to 5% when the number of test-takers is high? This would surely indicate that the indirect effect is minimal and that people do not have a good idea of whether they will pass in advance. Or that they are willing to take the chance even if they have a good idea in advances.

Whichever way you cut it, the presence of an indirect effect surely must show up in the pass rate to some degree.

What have we learned?

It seems logical that there is information in the pass rate about the degree to which the GAMSAT test can reduce the flow of new doctors compared to if the test did not exist.

In the real world, and not the hypothetical I described, the pass rate for the GAMSAT is about 20-25%. In fact, the pass rate is itself determined by a quota on new university places. The test doesn’t constrain new doctors because the university quotas do it, and that quota determines the passing grade and hence the pass rate.

The reason for explaining this is because this post is not about medical school. It is about town planning. The “entrance test” in the planning system is a planning application, which is required to (re)develop a property.

Many argue (e.g. point 4 here) that just because 90%+ of the planning applications are approved that this doesn’t indicate there is at most a small effect on the rate of new housing supply. They argue that the indirect effect dominates and that’s why the approval rate is high.

But this leaves us with a conundrum. We know that a property with a planning approval is worth a lot more than one without. Therefore there is a large payoff to getting an approval. Just like there is a large payoff to becoming a doctor.

Yet candidate medical students are willing to sit a test with a near 80% failure rate, often repeatedly, to get that payoff. However, property owners are not, even though the payoffs can be worth tens of millions of dollars or more.

While an indirect effect surely exists in both medical school entrance tests and town planning applications, the pass rate also contains information about the existence of this effect.

“There are two schools of thought… Science stands for healthy scepticism… asking for better evidence… Then you have a second school of thought that is public health… it has the stance that we have a crisis, we are like an army, the platoon must do this or that. Anyone who leaves the platoon must be shot down.”

I like the way John Ioannidis has characterised the COVID public health response. The science and scepticism approach has been overridden by the public health army approach, which has little need for evidence. I recommend his presentation in this video, which is the source of the above quote.

The two schools of thought might explain the “you are better than this” responses I sometimes get on Twitter when I raise concerns that the public health policy seems detached from the scientific and logical reality. I hope it’s because they want me in their army. I hope it’s not because they have given up seeking the truth.

For some reason, I have a brain that can’t stop trying to seek out contradictions and the underlying logic that makes sense of the world. Scientific scepticism seems hard-wired. For example, when I look at Australia’s superannuation system, logic forces me to conclude that the system as a whole makes funding retirement harder, not easier. So I say we should dismantle it altogether.

I predicted that house prices in Australia would rise in May last year and people scoffed. Someone told me I should hand back my degrees. But the underlying logic I saw was correct (or at least useful for prediction).

Being right when the mob is wrong is, unfortunately, never popular.

In fact, a good rule of thumb is that there is no new information when someone says something popular. There is a huge amount of information when someone risks their reputation to say something. This is why John Ioannidis remains one of the few experts whose words contain actual information. He risks his reputation to say them.

This blog post is about the scientific and sceptical school of thought on COVID policy. It provides a glimpse of the contradictions and the underlying logic I see at play. Some of my previous thoughts and comments on COVID policy can be found here.

Seeking logic and evidence

Vaccines are the path

The current marching song is that vaccines are the path to freedom. Recently promoted by the Grattan Institute, an 80% vaccination target gets discussed as the key to returning to normal life.

There are two problems with this. First, getting 80% of adults vaccinated is quite difficult and has only been achieved in a small number of places.

Second, highly vaccinated places are getting COVID, some more than at any time before (e.g., Iceland, Israel, San Francisco, with surely more to come). While vaccines appear to be reducing mortality rates from COVID, differentiating the effect of the vaccination from the effect of previous population exposure is quite a challenge.

It seems to only make sense to vaccinate the elderly given the risk relativities and the limited effect on transmission.

Blaming one side of politics or the other for the “botched vaccine rollout” looks like nonsense to me when the experience elsewhere is that the level of vaccination is not having a major effect on subsequent virus waves.

Masks work

The only problem with this idea is that you cannot see it in the population-level data. In fact, you cannot even see much evidence that masks work in surgical theatres. Here is a thread containing many studies showing they don't.

Masks have become political symbols. And people love it.

The seasonal resurgence of COVID across the US despite vaccination and masking is quickly turning into a political problem to be manoeuvred around, not a health issue. Yet more signs that COVID policy is not health-driven.

Vaccine passports

Another chant I hear is that vaccine passports are necessary. But if vaccines work, we do not need a vaccine passport. The vaccinated are not at risk and their presence in the population reduces virus spread regardless. If vaccines do not work, then a vaccine passport is not stopping the virus from circulating and spreading amongst the vaccinated.

Notably, the recent data shows that vaccines wear off and vaccinated people get COVID at quite a high rate compared to unvaccinated (perhaps as much as 80% after six months) and are likely to transmit at a similar rate. This is why vaccine boosters are being planned.

I cannot see how the current crop of vaccines gets anywhere near a reasonable benchmark for restricting movement. Most people when pushed seem happy that vaccine passports would be used as an incentive to get vaccinated rather than as a direct health measure.

R0 talk and “exponential” threats

Despite a high reproduction rate and infectiousness, many COVID Delta waves have fallen off dramatically with relatively low infections (e.g. India). R0 does not seem to give any indication of the final size of an outbreak.

Another big unknown in the modelling is the degree of prior immunity in terms of the variation in COVID waves over time and between regions (such as if previous local viruses conferred some protection in the population), and in terms of potential for reinfection.

Lockdown cost-benefit

The lack of discussion about costs and benefits from masks and lockdowns is mass willful blindness. When an attempt is made, or some concession is made that the approach of evaluating costs and benefits is sound, usually another panicked argument is substituted instead.

Way back in the early days of COVID we saw some appalling attempts at cost-benefit analysis. One was out by a factor of 1,000! You could not be more wrong if you tried. Despite this, these same people are pretending to have been right all along and are still being taken seriously by the media.

That basket case Sweden

Sweden had a roughly 5% increase in total deaths in 2020 with no vaccine and no lockdowns (98,000 against ~93,000 expected deaths). For context, total deaths increased 5% in Australia from 2015 to 2017 (144,000 compared to 137,000 due to a 1.5% increase followed by a 3.5% increase).

Sweden saw no increase in deaths in any age group under 50 years.

When faced with these facts some say Sweden did reduce mobility voluntarily and that made the difference. But this merely implies that compulsory masks and mass lockdowns are not necessary and do not make a difference. You cannot have it both ways.

Kids and vaccines

Plenty of medical experts and ethicists warn about the risks of vaccinating children. They are rightly cautious. If one death per million from the AZ vaccine applied to Australian children that would kill 7 kids if they were all vaccinated. How many would it save? Given the low risk of COVID in children that number seems to be roughly 14 to 20. Are you happy with that trade-off?

This paper estimates the likely range of vaccine-related deaths if 80% of 18-59 year olds are vaccinated at 17 to 153. Given how little vaccines seem to stop virus transmission these risks need to be carefully assessed.

Suicides

A concern of mine has been that lockdowns would result in a rise in suicides. Thankfully that has not happened, but that does not mean there is no harm from lockdowns. U.S. data is showing a 50% rise in emergency department visits by teenage girls involving suspected suicide attempts.

The material prepared for quarantining households is predicated on the fact that forcing people to stay in their homes for weeks on end will lead to people bashing each other. Recent surveys of domestic violence care agencies suggest this has been the case.

Surveys show huge increases in depressive symptoms during lockdowns. These human well-being costs are real.

Media reporting for the army

I want to also demonstrate how easily the media falls into line with the public health army.

You may have seen the below chart showing that death from the AZ vaccine is less likely than being killed by a lightning strike in any year. Did you ever question it?

I did not at first either. But once your logical mind is brought into action you have to ask some questions. This is a classic example of the media picking and choosing “facts” and repeating them until they become the truth. Here’s the AMA President repeating it. Expect to hear it in casual conversation.

But there are two problems with this “fact”. First, the AZ vaccine has seen 7 deaths in Australia from roughly 7 million doses, so that risk is closer to double the 0.5 per million presented. Much more for all side-effects. Second, a risk of 0.4 per million for lightning strikes implies about 10 lightning strike deaths in Australia per year. But in reality, it is usually less than 2 (average of 1.9 for the past decade). So this is overestimated by a factor of five.

These two corrections mean that the AZ vaccine is ten times more likely to kill you than lightning. This “fact” is off by a factor of ten. The vaccine risk is still low. But this is hugely misleading and certainly is not going to promote trust in authorities when the error becomes more widely known.

Do you think the author of the original article presenting this “fact”, or the editors at The Conversation, actually care? Nope.

I have been reliably informed that someone with a keen eye for statistics approached the author to request they update the chart with more accurate statistics (their original lightning strike stats were simply lifted from here). But no. No action. The editors prefer to keep the wrong statistic on this hugely important topic rather than issue a small correction. Off by a factor of ten is totally acceptable as long as you are marching with the public health army.

And what of the risk of people dying with COVID? Why not put that on the chart and make a decent comparison. There has been almost no attempt at putting COVID risk in context in the media.

Perhaps the reason is that the data doesn’t sing to the public health army marching song. Take the Swedish data again. For ages 0-19 the risk of dying from COVID after 18 months of community transmission including two waves of infections, mostly with no vaccine, masks or lockdown, was 3.7 per million (9 deaths out of 2.4 million population). On an annual basis that is 2.5 per million. If we partition the data to account for co-morbidities, a healthy young person’s risk of COVID death gets much lower. Lower than the one in a million risk from the AZ vaccine? Probably not. But not a big difference, and certainly not enough difference to warrant the calls for rushing to vaccinate children.

Another place the media seems to be wrong is the story that vaccines produce better immunity than recovering from COVID. You might have heard this or seen a tweet like this.

So let us check the source of this claim. Nope. The study has no comparison between recovery-induced immunity and vaccine-induced immunity. It does show that some well-known immune responses do wane over time after infection. But this natural immune response may still be more persistent than the response from vaccines. However different evidence would be needed to establish the relativities. That doesn't stop the authors from making this claim, which is strange considering that one of the findings is that there is a subpopulation of people with a super strong and persistent immune response. Could they be simply chanting the public health army marching song?

Predictions

All of this has been a long-winded way of saying that a lot of what you hear about COVID and vaccines and the effect of our policy choices is incomplete, misleading, or plain old wrong. The one part that does make sense is quickly getting vaccines to the elderly—the overwhelming evidence for this conclusion is why every place is doing it regardless of differing views on masks, lockdowns, vaccine passports or border controls. In my view, vaccinating the elderly is one of the few policy actions the evidence favours.

The rest of the actions only make sense if you are in the business of marching a public health army and don’t care where that army is going or how many of its own it loses along the way. Lockdowns cost a huge amount of lives, masks don't do anything at a population level, and vaccine passports make no sense given the type of vaccinations available.

If the underlying logic of COVID I have identified is roughly true, then I should be able to make some predictions. Here are some.

There will be a time in the next two years when Australia has a much bigger COVID outbreak than any yet despite being hugely vaccinated. Depending on the political fallout from 2021 we may even collectively take no action. No masks. No lockdowns. No border closures.

Australia will see a year with a 7% increase in all-cause deaths (about 10,000) in the next decade and no one will notice. Given the ageing population and the normal variation in deaths each year, this makes sense. I’m actually being intentionally bold on this prediction. Realistically a 5% increase (7,000 extra deaths), or 134 extra deaths per week, is more likely to be observed.

Vaccine passports of some sort will be enacted against all evidence. They will be cheered by the mainstream media as they justify all the terrible policies the public health army has forced onto us so far. No one will care that the vaccines wear off or that the vaccinated transmit the virus to a similar extent after six months or so. The public health army will march on from the vaccine race song to the vaccine passport song, to whatever else keeps the marching going.

How the analysis looks to me

There is a spoof viking show called Norsemen on Netflix. In it, the characters talk about customs of life and death in a hilarious matter-of-fact way. I feel like I am living in a spoof Netflix show. The wonks are arguing the finer points of how to skin a virgin alive to please the gods while I stand by looking at the evidence that suggests rejecting the premise altogether. If only our policy choices today were a laughing matter.