Henry Halloran Trust, The University of Sydney

20 March 2020

Download proposal as a PDF

- We propose that State governments (or Federal) create a “Central Housing Bank” (CHB) that stabilises the housing construction sector by swapping assets, in this case, cash, for new dwellings. Just as the Central Bank swaps cash for other financial assets to solve liquidity problems in financial markets, the CHB would do the same for one of the nation’s largest economic sectors.

- As a national program, a dwelling target for the first year could be 30,000 dwellings across the 20 largest towns and cities in the country (around 0.5% of the number of dwellings in these towns). This is roughly 15% of the new dwelling completions in 2019, a significant demand buffer for the housing construction industry, supporting an estimated 150,000 highly productive jobs.

- In balance sheet terms, these actions are costless for any government that undertakes them, as they receive a dwelling of equal (or perhaps higher) value to the cash they give up. Margins on housing development are typically above 25%, so this would be an opportunity for a public agency to engage in discounted counter-cyclical asset purchases to support jobs in the construction sector.

- The CHB can then use those acquired dwellings in a number of ways to support policy objectives, such as

- renting in the private market to help stabilise rents,

- using them for public housing at discounted rents,

- selling to social housing providers at discounted prices,

- or selling to the private market in future periods when prices are rising to dampen the housing cycle.

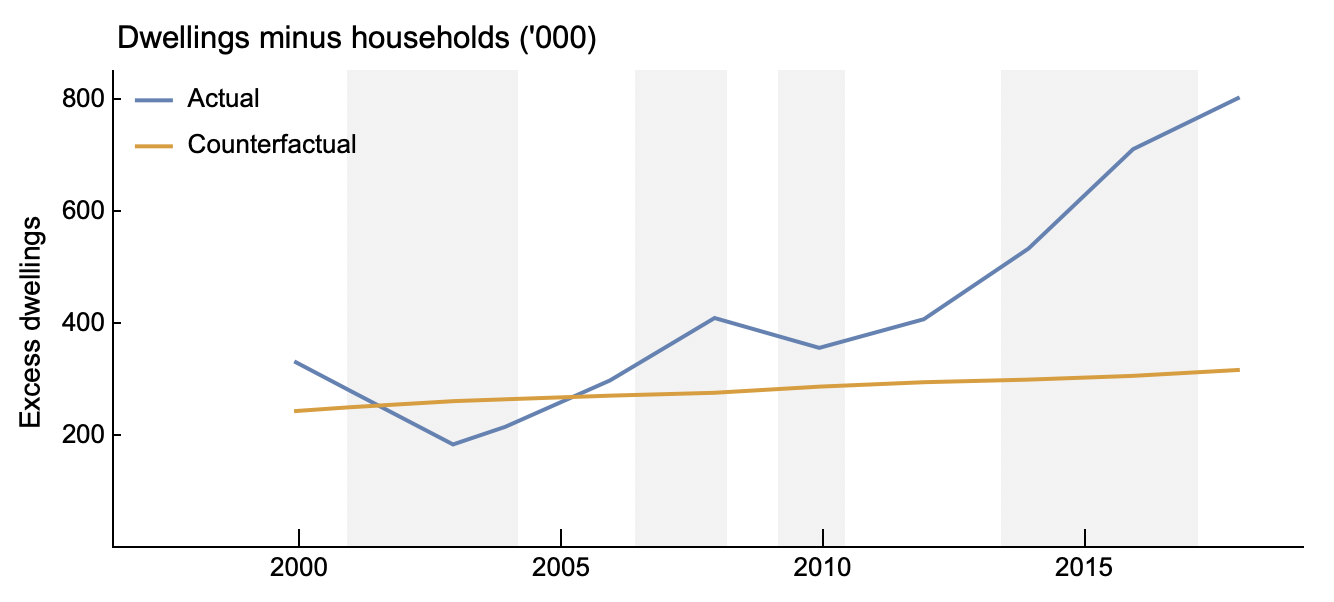

- Housing construction investment is a volatile, but productive, part of the economy, currently accounting for around 5% of GDP and 7% of Australia’s workforce (including housing construction and ancillary industries).

- Ensuring continuity and utilisation of productive organisations, such as builders, manufacturers of construction materials, and the design and management professions, can help ensure productive capacity is maintained during the crisis, and in the post-crisis period.

- The basic implementation of a CHB would be as follows:

- Employ a small group of senior construction and project management experts to manage the CHB, ideally from the non-housing construction sector, such as mining and oil (to avoid conflicts of interest).

- This CHB team would request tenders from private housing developers or landowners to supply new apartments at an agreed price. The objective is to utilise the pipeline of already approved housing developments to speed up the process. In Sydney alone, there are an estimated 20,000 approved yet not-yet-commenced dwellings. Nationally, the top eight housing developers have a landbank of over 200,000 apartments and houses. There is a massive pipeline of sites that the private sector has queued up for housing that they will be looking to sell to reduce exposure to falling land prices.

- They could also shop for development sites as a market participant.

- The CHB management team would be incentivised to meet dwelling supply targets both in terms of the quantity delivered, and the location-adjusted average price paid. Independent assessment by State Valuers, in conjunction with State or Federal Treasury, can determine the value for money and hence the performance bonuses of the management team.

- Rough annual new dwelling purchase targets for the CHB could be set as a schedule across major towns and cities in proportion to their population, for example, 0.2% of the population in every town or city above 100,000 residents (of which there are 20 towns and cities nationally). Expansion to smaller towns can be conditional upon the success in the first three years of the CHB. This would be roughly 30,000 dwellings in the first year.

- There are enormous macroeconomic stabilisation benefits of this system. The accumulated stock of rental housing owned by the CHB can be used to dampen housing price upswings by introducing a selling rule. For example, if dwelling prices begin to rise above a set rate, of say 5% per year, this would trigger sales of the stock of dwellings held in that region to private sector buyers at the rate necessary to keep growth below the target rate (again, like Central bank intervention to stabilise interest rates), absorbing speculative demand and stabilising housing prices.

- This system is not dissimilar to housing systems in Singapore, and public housing systems in Europe, and previous housing systems in Australia and North America.