Article first appeared at MacroBusiness

The US economy has shown some signs of stabilisation over the past few months. For example, retail spending appears to be revisiting a growth path. According to some commentators, the US economic green shoots appear robust and healthy, while I remain cautious about projecting anything more than muddling though, with a drawn-out grinding improvement in employment as the consumer debt burden is reduced by inflation, repayment and default.

The US ‘recovery’ is the result of many factors, including the relatively cheap US dollar (the US TWI is back at levels last seen in the mid 1990s), but importantly, and often overlooked in financial discussions, relatively cheap domestic energy fuel prices. WTI crude is hovering around $100/barrel, still 25% down on the pre-crisis boom period.

But the key energy consideration for the US recovery, and future US political–economic trade policy, is the current domestic natural gas boom which has meant the US has shifted from gas net importer to net exporter.

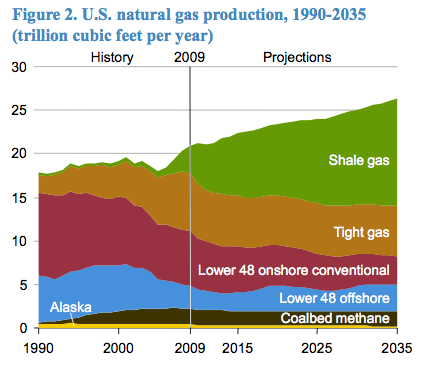

Below we can see the recent rise in natural gas production, mostly as a result of the emergence of economical shale-gas extraction, for the past three years or so. With natural gas comprising a quarter of domestic US energy needs, the scale of this boost in energy supply is significant. Some have gone so far as to suggest that the natural gas boom, as a result of fracking and coal seam technology, is leading to a ‘new world energy order”.

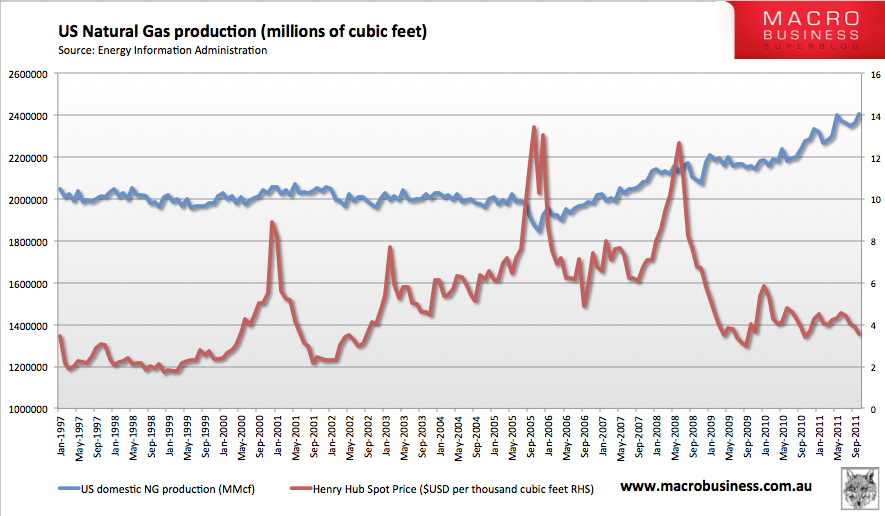

We can also see that the US domestic spot price for natural gas has remained quite subdued in this period due to a combined of demand destruction, particularly during the financial crisis period between 2008 and 2010, and increased domestic supply.

The US government closely regulates natural gas exports, and any import or export of natural gas requires approval of the Department of Energy, as per Section 3 of the Natural Gas Ast 1938. (approvals in progress are here).

Debate is now brewing over the direction of US energy policy in the treatment of export approvals for the natural gas glut, given the significant profits to be made from liquefaction and export to Asian markets.

As the Wall Street Journal notes:

The U.S. already exports some natural gas, mostly via pipeline to Canada and Mexico. A recent wave of export proposals by energy firms seeks to liquefy gas and ship it overseas in tankers.

U.S. natural-gas prices have fallen below $3 per million British thermal units, pushed down by swelling production that became possible with the advent of new drilling technologies. With prices so low, U.S. producers are eager to reach customers in other parts of the world, such as Japan, that pay three to four times as much as U.S. users.

Collectively, they want to ship out about 14 billion cubic feet of natural gas a day, roughly 20% of current U.S. production.

But some lawmakers on Capitol Hill are opposed to increased exports and are urging the Department of Energy not to issue the required permits. The department will use the findings released Thursday in making its decision.

The administration is reviewing the export proposals “to ensure they are in the best interests of American taxpayers,” Energy Department spokeswoman Jen Stutsman said.

One argument is that maintaining a tight limit on exports will keep the domestic price low, and domestic energy intensive industry more globally competitive:

The estimate by the Energy Information Administration, which compared gas-price projections in given years with and without higher exports, appeared to bolster assertions by U.S. manufacturers that they could face stiffer prices for natural gas and lose a competitive edge over companies abroad.

“Higher levels of exports would certainly impact the manufacturing recovery that has been revitalized in the U.S.,” said George Biltz, Dow Chemical Co.’s vice president for energy and climate change. “Exporting too much natural gas simply exports well-paying U.S. jobs.”

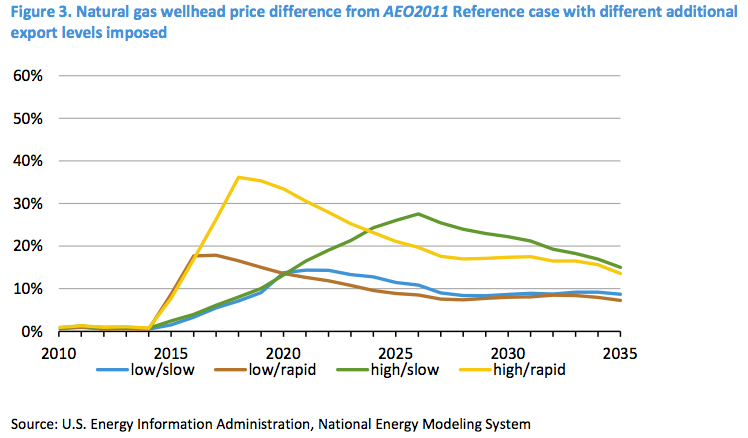

US Energy Information Administration (EIA) analysis of price impacts from increased exports shows that, under various scenarios, of high and low growth paths for shale-gas production, and rapid and slow scale up to exports, domestic price increases could be in the order of 15-35%, depending on the speed of development of export capacity. See their chart of model results below.

As secondary concern has been whether exposing US domestic natural gas production to the global market will import price volatility due to global events. If export capacity is high enough, this may be the case. But if export capacity is limited by physical capital – the number and size of pipelines, and finite capacity of LNG conversion and loading facilities which would require a decade or so lead time to expand – then domestic prices will not capture global volatility, as high prices cannot be passed through to the domestic market.

The big question for US energy policy, is how best to share the benefits of this new energy supply. The way I see it, maintaining tight control on export markets keeps prices for domestic gas users at a globally low level, making a diverse range of US industries more globally competitive. However, this benefit comes at a cost to the gas industry that is being denied access and profits from global markets, such as Japan, Korea, China and India, where gas prices are significantly higher.

Indeed, allowing exports would in a way provide economic benefits to the destination countries, as the global price of LNG will be reduced as the increased supply comes on board. For Australia, where the infant Coal Seam Gas (CSG) industry is being relied upon as a driver of economic growth, increased global competition in the gas market from US exporters may be cause to pull pack some of their price forecasts in the short term. Last week, Fitch placed the entire sector on negative watch for this reason among a growing list of other negatives.

The current US debate is interesting from the lens of an Australian resource State, where almost all energy resources are developed for export markets. It is surely inconceivable that Australian authorities would consider such regulation to ensure competitiveness among our own industry. (Although, as mentioned earlier, the ability for export markets to compete with domestic energy markets is dependent on the interconnection of the supply chain.)

It is worth keeping a close eye on how US energy policy plays out in the treatment of the shale-gas boom, and the potential implications for LNG markets globally.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter@rumplestatskin