I wrote once before that the concept of waste has been distracting environmentalist for decades. Today I came across this exceptionally interesting article on food packaging. The main point is that packaging serves an important purpose - to preserve food. The longer food is preserved, the more likely it is to be eaten rather than wasted. Thus, packaging cuts down immensely on food waste.

I do however believe that some packaging, such as the excessive size of cereal boxes to ensure good shelf space, does not always result in benefits for consumers.

Tuesday, February 9, 2010

Monday, February 8, 2010

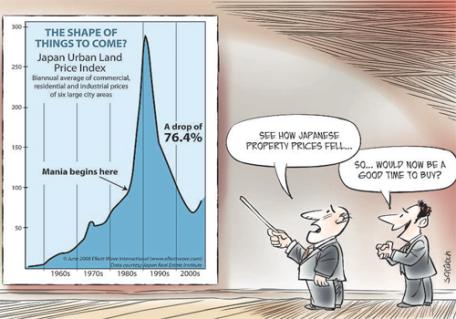

Fail: CPI, housing and the cost of living

This short article about inflation, and the ABS review of the Consumer Price Index (CPI), prompted me to write again on the subject. In fact, some friends and family who recently returned from a few years abroad have also been bugging me about why Australian prices have shot up so much, yet we hear almost nothing about rapid inflation. Housing prices in Brisbane have typically increased 200% in the past decade - around 7% per year. If housing was just 10% of the CPI basket, it alone would contribute 0.7%pa growth to the index.

Unfortunately, not many people know that the CPI does not measure the change in the cost of living (see p6 of the ABS CPI overview report here). The ABS method, including quality adjustments and the weighting of household consumption goods, means that the CPI fails to be a useful measure for determining real incomes and purchasing power.

Thursday, February 4, 2010

Randomness and probability: can people intuit probability?

One of my concerns with the evidence on the misinterpretation of randomness and probability in The Drunkards Walk arises during the discussion of the first law of probability: The probability that two events will both occur can never be greater than the probability that each will occur individually. While the law makes intuitive sense, the evidence that people fail to apply it to their reasoning is a little flimsy.

Mlodino asks us to consider an experiment from Khaneman, Slovic and Tversky’s famous book on judgement under uncertainty. Given the brief description about the Linda below, eighty eight subject were asked to rank the statements that follow on a scale of 1 to 8 according to their probability, with 1 representing the most probable, and 8 the least. The results are in the order ranked by the participants from most probable to least probable.

See the results under the fold and why their finding, that people have poor intuition of probability, may be incorrect.

Mlodino asks us to consider an experiment from Khaneman, Slovic and Tversky’s famous book on judgement under uncertainty. Given the brief description about the Linda below, eighty eight subject were asked to rank the statements that follow on a scale of 1 to 8 according to their probability, with 1 representing the most probable, and 8 the least. The results are in the order ranked by the participants from most probable to least probable.

See the results under the fold and why their finding, that people have poor intuition of probability, may be incorrect.

What I've found interesting lately...

There has been a lot of comment on bonuses in the banking industry since the onset of the GFC. Read Dan Ariely's take on the effectiveness of bonuses here.

For those who believe that economics generally gets things half right, behavioural economics might be your thing. A mix of psychology and economics, this field has been enlightening economists for the past two decades. Some of the latest findings in behavioural economics are found here (highly recommended).

For those who believe that economics generally gets things half right, behavioural economics might be your thing. A mix of psychology and economics, this field has been enlightening economists for the past two decades. Some of the latest findings in behavioural economics are found here (highly recommended).

Wednesday, February 3, 2010

Ugly city syndrome

This article suggests that ugly cities are the result of poor political leadership. That seems like a long bow to draw. I believe the cause of ‘ugly city syndrome’ is more subtle, and maybe we just have ourselves to blame. The simple answer might be that in the modern day of cheap international travel we are comparing ourselves to a wider selection of cities.

But where are the incentives to create a beautiful city?

But where are the incentives to create a beautiful city?

Monday, February 1, 2010

The Australian property market debt gamble

Investing and gambling are often mistaken for each another. In one, you take risks based on known probabilities, in the other, unknown probabilities. In one, you will probably win in the long run, in the other, you are bound to lose out. In both pursuits we are psychologically predisposed to scams.

I find it interesting that prudent advice for gamblers is to risk only your own money, while for investors it's a different story - the more leverage the better. But there must be an optimal level of leverage, otherwise we would all simply continue to borrow and destroy the value of the currency through money creation.

Given the realities of our world, one would expect that leverage below this optimal level would not persist for an extended period, as people would begin to notice the advantages of more leverage, nor would leverage or debt beyond this optimal level be able to persist. It is therefore interesting to ask how would we know if we are above this optimal level?

Thursday, January 28, 2010

UPDATE - How not to climb the property ladder

I really appreciated the discussion on my last post, and wanted to clarify some of the issues raised.

My two key points were:

1. The capital gain made from buying a cheap home and upgrading later does not always improve your ability to buy a larger place in the future, and

2. That forgoing life's little luxuries to start a savings plan directed at owning your own home is not always effective. The 'work hard and save' mantra does not work if prices increase faster than your ability to save.

The issues flagged by readers were that

1. I ignored increased wages

2. I ignored the paying down of principle, and

3. I ignored the fact that rents increase in line with CPI while loan repayments do not.

My response is under the fold.

My two key points were:

1. The capital gain made from buying a cheap home and upgrading later does not always improve your ability to buy a larger place in the future, and

2. That forgoing life's little luxuries to start a savings plan directed at owning your own home is not always effective. The 'work hard and save' mantra does not work if prices increase faster than your ability to save.

The issues flagged by readers were that

1. I ignored increased wages

2. I ignored the paying down of principle, and

3. I ignored the fact that rents increase in line with CPI while loan repayments do not.

My response is under the fold.

Tuesday, January 26, 2010

How not to climb the property ladder

I am one of those generation Ys looking to buy my own home, and from this perspective, it is not quite that simple.

The mythical property ladder

The argument that if younger generations decreased their expectations, and maybe bought a small apartment now, so that they could somehow work their way up the ‘property ladder’, is entirely misleading.

For example, a young couple buys an apartment for $200,000 in lieu of a $400,000 house they really want based on the contemptuous advice of older generations. They imagine that in 10 years they might be able to sell for $350,000, netting a profit of around $100,000 to spend on a larger home (after transfer costs). The problem is that larger homes have also increased in price by 75%, so that the $400,000 house is now $700,000. Buying that dream home has gone from a $400,000 prospect to a $600,000 prospect even with the apparent advantage of being on the property ladder.

The way to benefit from increasing property prices is to buy multiple investment properties, so that you leverage the benefits beyond your single dwelling needs.

No more avocados

Next, we can look into the arguments about spending a little less on luxuries to get a person into a home-buying financial position. Dining out, gadgets, and holidays all seem to get mentioned. But if we look into it, these relatively small expenses are not the main factor – the main factor is income.

A hypothetical future home buyer might spend $200 per week on dining out, ‘gadgets’ (mobile phones etc), and travel. That’s $10,400 per year – maybe $3,000 on a trip to SE Asia, $2,000 on gadgets, $2,000 on dining out, and the balance for other luxury items. Let’s see what that money could have done if it were funnelled into a property-buying strategy.

Assuming a starting point with no savings, this hypothetical person (or couple, or family) can save about $58,000 in 5 years assuming they receive 6% on their savings. If they thought they might one day want to live in a home that currently costs $300,000, by the time they save their $58,000 the home is worth $400,000 (at a 6% price growth rate). They now need $80,000 for their deposit. They continue saving instead of splurging and in another 5 years they have $137,000 saved. The home is now worth $535,000. They have enough for a deposit, but the repayments on their home and associated ownership costs are now around $900/week.

So after ten years of saving, living life without those luxuries that make it so much more enjoyable, they are in no better a position than before.

I’ll leave you with a question. If you bought a home for $100,000 in 1990, and the market his risen so that it is now worth $600,000, how much better off are you?

Sunday, January 24, 2010

How randomness rules our lives and why statistics need discipline

I feel the need to share some of the most interesting insights, and highlight some of my remaining concerns about the nature of randomness and probability. My main reason for caution is because the normally practical and insightful discussion occasionally crosses the boundary between mathematical and statistical insight and plain old common sense. These instances reiterate my stance that statistics need discipline. For now I will put these to one side – topics for future posts. Today I want to share one of the more interesting insights into differentiating luck from skill with some basic probability theory.

Tuesday, January 19, 2010

Helmet law rebound effects and the success of terrorism

I write regularly about rebound effects - those unintended consequences that occur due to behavioural adjustments. I wrote my Master’s thesis on the rebound effects from energy efficient technologies and household energy conservation behaviour (a good summary is here, my thesis is here, a draft paper on household conservation is here, and a draft paper on the effect of government environmental subsidies is here)

I have written about rebound effects from using photovoltaic panels. The rebound effect from recycling, which enables us to use even more of the raw material we are trying to conserve. Recently, I wrote about the potential rebound effect from sunscreens – because we don’t have the immediate signal of sunburn to tell us that we have had enough sun exposure, we tend to spend more time in the sun.

One area I am particularly adamant that unexplored rebound effects exist is in preventative health care costs – by preventing one disease, we enable people to succumb to other diseases, which have potentially greater treatment costs.

But these sly rebound effects do not end there.

Subscribe to:

Comments (Atom)