The continued media hype around Australia’s economic stability and security can be partly attributed to the fact that, by official figures, we avoided a ‘technical recession’ during 2008/09, and also that ‘the health and strength' of Australia's banking system played a major factor in domestic economic outcomes following the financial crisis (here for example).

Griffith University’s Professor Tony Makin, however, has a little more to say about whether Australia actually avoided recession. The answer depends on your definition, and we are unique in that respect.

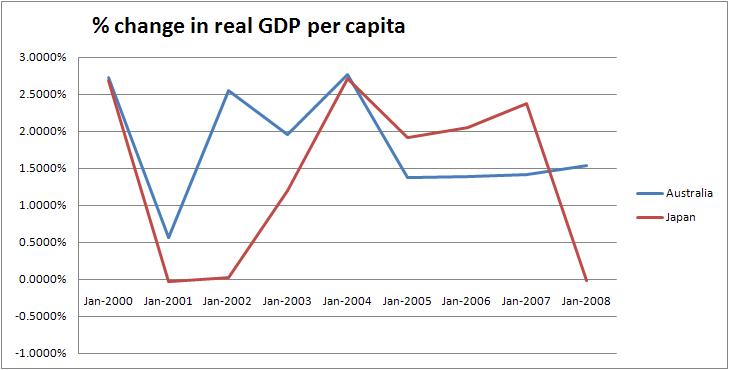

In the aftermath of the GFC in September 2008, Australia's nominal GDP, real GDP measured on an income basis and on a production basis, as well as real GDP per person, all fell over two successive quarters, as did various other national income measures that account for the slump in export commodity prices (or terms of trade) at the time.

Of the many national accounts series the Australian Bureau of Statistics publish, the only one indicating there wasn't a recession was the real, or price level adjusted, national expenditure series.

In the US, a recession dating committee of the National Bureau of Economic Research uses a battery of macro-economic measures, not just the somewhat arbitrary two successive quarters of negative real GDP.

If the behaviour of Australia's business cycle in the aftermath of the GFC had been assessed by an independent committee of economists with reference to a broader range of macroeconomic indicators in this way, a recession, albeit mild, would most likely have been declared for 2008-09. But this would not have been of great concern because, due to greater labour market flexibility, unemployment did not rise anywhere near as much as in the recessions of the early 80s and early 90s.(here)

No doubt business people would have wondered how official figures could have been so out of touch with on the ground realities during early 2009, but a mere statistical discrepancy kept the headlines optimistic.

And as far as the ‘health and strength’ of our banking system, well, let’s just say a better phrase would be ‘government rescue’ of the banking system, with the deposit guarantee and massive fiscal and monetary stimulus.

All around the country, banks were facing unusual demands for cash. Small businesses in Queensland and Western Australia were switching their deposits from regional banks to accounts with the big four banks.

An elderly woman turned up in the branch of one bank in Queensland with a suitcase and asked to withdraw her term deposits of $100,000 or more. Once filled, she took the suitcase down to the other end of the counter and asked that it be kept in the bank's safe.

A story did the rounds of the regulators about a customer who wanted to withdraw his six-figure savings. The branch manager said he did not have that quantity of cash on hand, but offered a bank cheque, which the customer accepted, apparently unaware that the cheque was no safer than the bank writing it.

It was a silent run, unnoticed by the media. Across the country, at least tens and possibly hundreds of thousands of depositors were withdrawing their funds. Left unchecked, there would soon be queues in the street with police managing crowd control, as occurred in London at the Golders Green branch of Northern Rock a year earlier.

...

Households pulled about $5.5bn out of their banks in the 10 weeks between US financial house Lehman Brothers going broke - the onset of the global financial crisis - and the beginning of December. That is roughly 80 tonnes of cash salted away in people's homes. Mattress Bank is doing well, was the view at the Reserve. A year later, only $1.5bn had been put back.

The worst problems were in the second-tier banks, particularly Queensland's Suncorp and, in Western Australia, Bankwest. Deposits at the big four banks were surging as customers sold their shares, pulled money out of cash management trusts and put the proceeds in the bank. But at Suncorp deposits slumped by $1bn. They dropped $2bn at Bankwest.

The regulators and the government were gravely concerned for these two banks. Suncorp had total assets of $75bn and Bankwest $60bn. Bankwest was in double trouble because its British parent, HBOS, was teetering on the edge of bankruptcy.

...

Despite their preparation, the Lehman crash caught local banks by total surprise. NAB chairman Michael Chaney had set off on a 13-day rafting trip down the Grand Canyon on the day Lehman failed. He had taken a satellite phone but by the time he got it to work his share price had collapsed by almost 30 per cent. "I couldn't get a helicopter in there, so it was a five-hour climb out," he says.

Balance of payments figures show that in the immediate aftermath of the crash, Australian banks were called on to repay $50bn in short-term debt to international investors who refused to roll over their exposures.

Governments across the world were also being tested. Two weeks after the Lehman crash, Ireland's banking sector was facing an alarming run on larger deposits. The government stepped in and guaranteed all deposits and wholesale fundraising.

There was an immediate call for the British government to follow suit. Within a week, Germany, Denmark and Greece had offered unlimited deposit guarantees, while the British and a number of other European governments had increased the size of their insurance schemes. The Reserve Bank, APRA and Treasury were worried as were the chief executives Wayne Swan was talking to.

The long-standing concerns of the main banks about depositor protection were cast aside. The fate of small institutions could influence the stability of the system.

"One of the lessons of this whole period is you can have an abstract almost clinical discussion in the absence of a crisis about which institutions are systemically important and which are not. But when the crisis hits, is there any financial institution that is not systemically important?" Henry says. "It was my view back in September after the collapse of Lehman, I came to the view there was no financial institution in Australia that could not be regarded as systemically significant."

The issue was so delicate that most cabinet ministers knew nothing of what was going on.

"Some of this stuff is so sensitive, the bank guarantee could only be agreed between the Prime Minister and myself," says Swan. The government's unlimited guarantee of retail deposits went further than any other country, partly because Treasury was now concerned about capital flight.