This post first appeared at Macrobusiness

Not a day goes by when some economic commentator notes the ‘decoupling’ of economic growth of the developed and emerging economies. Europe looks almost certain to have a 2012 recession, and the US continues to have doggedly high unemployment with very soft conditions all around. Brazil, Russia, India and China, the BRICs, are meant to be taking up the slack, especially with domestic demand in China, to keep global growth on track.

But just as my suburb has a hard time decoupling from the rest of the city with which we trade our goods and services, the BRICs are nestled solidly in the layered courses of the integrated global economic masonry.

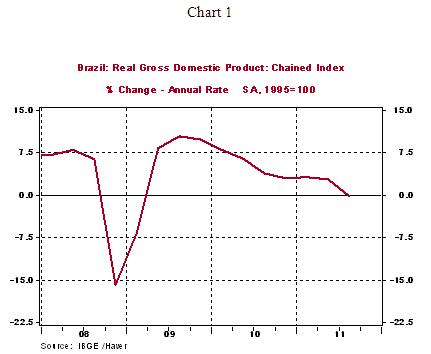

In the least reported economic news of the month, Brazil’s GDP was flat in the September quarter. During 2010, Brazil’s economy grew 7.5%, while the year to September 2011 saw a mere 2.1% growth, with an obvious trend – down. I am not sure what is on the horizon turn this around for Brazil, apart from a surprise boost in economic activity in Europe and the US (chart from here):

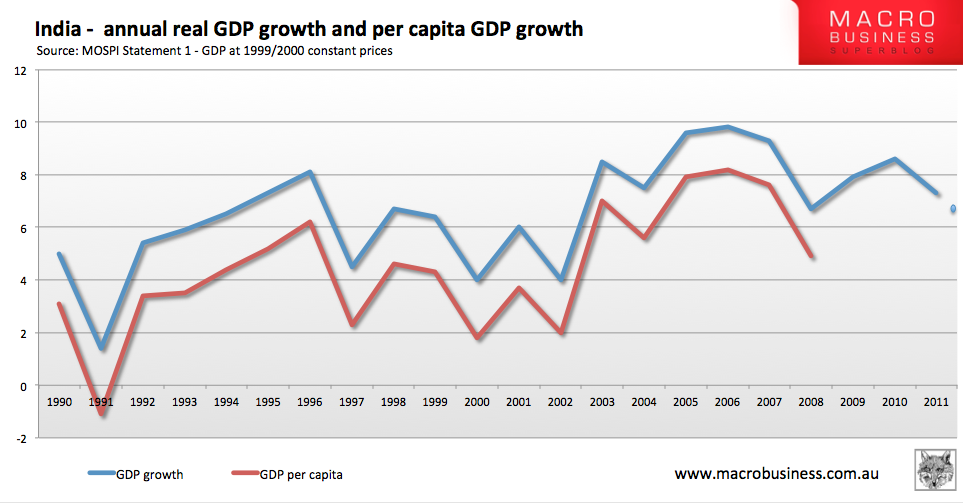

India was expected, much like China, to continue to grow at double-digit rates, but has just recorded its slowest GDP growth for two years, at 6.9%. Particularly:

The manufacturing sector, which contributes nearly 16 percent of GDP, grew at a measly 2.7 percent, down from 7.8 percent a year ago. Agricultural output rose an annual 3.2 percent for the same period, down from5.4 percent a year ago.

The worst hit was mining, which showed a decline of 2.9 percent after growing by 8 percent in the same period last year.

Here is how Indian GDP growth has looked since 1990, with the September annual measure marked in addition to the annual measures:

The trend path for growth in India is looking to be heavily influenced by external factors. Of course, exports make up about 20% of the Indian economy, so one must take external conditions into consideration. Further, around 32% of the Indian economy is involved with capital investment, which can be easily scuttled should prevailing global market conditions render the financial returns unattractive.

Russia is bucking the trend a little, with GDP growth up from 3.4% annual in the second quarter, to 4.8% over the year to September 2011. Currently this appears stable, but relatively slow.

Which brings us to China. Well, I’m not sure what more I can add on China, but the image below shows that growth is remains high, but is doesn’t appear to be taking off in a hurry. Annual growth has been steadily falling for the past 18 months, from 12% in early 2010, to 9.4% in the latest data:

I am not one to criticize a bit of economic stability, and the higher rates of growth on a lower base do mean that the share of economic expansion of the BRIC is relatively high. But with these levels of growth I can’t see how the BRICs are meant to support the waning demand of the much larger western economies. In terms ofshares of the global economy, Japan is 8.75%, US at 26%, the EU15 at 26%. For the BRICs, Brazil is 2.4%, Russia is 1.9%, India is 2.3% and China is 7.5% – or 14.1% in total for the BRICs.

For some more perspective, the US military budget is about $1trillion pa, or half the size of the Brazilian economy, or two-thirds the size of the Russian economy.

Clearly, very strong growth rates from such a small economic base would be required to counteract even very moderate contractions in the developed world, and this is not visible in the trends we are seeing. You can’t simply decouple the globally integrated economy while capital and goods are traded freely.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter@rumplestatskin