For an environmental economist these words are blasphemous, but I said them, and I have good reason to.

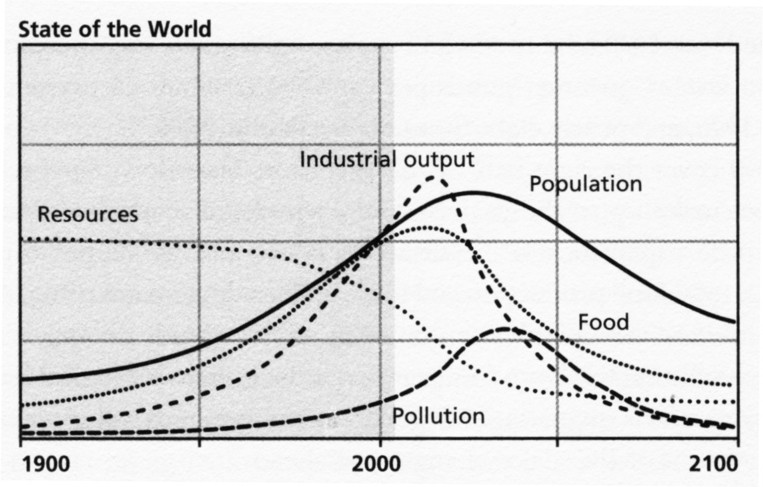

The modern Limits to Growth movement gained prominence with the publication of the Club of Rome’s book of the same name in 1972. This book, by Donella Meadows and colleagues, reports on the results of a computer simulation of the economy under the assumptions of finite resources. The World3 computer model produced scenarios showing that under various assumptions, a decline in non-renewable resources will lead to a decline in global food and industrial production, which will in turn lead to a decline in population and greatly reduced living standards for all.

The following image is one example of the results of their simulations where a catastrophic decline in industrial output, food production and population will result form reaching our finite resource limits.

While I don’t doubt the finitude of many natural resources, and that the human population cannot grow indefinitely, I doubt that finite limits of resource inputs to the economy necessarily means that economic growth cannot continue indefinitely.

To be sure, I am certain that substantial unforeseen changes to the rate of extraction of some resources will lead to short-term disruption of established production chains, such as shocks to oil supply, but in the long run I see no reason that an economy with finite resource inputs cannot increase production through improved technology and efficiency.

I need to be clear that when I talk of economic growth I mean our ability to produce more goods and services that we value for a given input. Increasing the size of the economy by simply having more people, each producing the same quantity of goods, will be measured as growth in GDP, but provides no improvement in the material well being of society.

A better measure of growth is real GDP per capita. This adjusts for the disconnection between the supply of money and the production of goods, and adjusts for the increase in scale provided by the extra labour inputs. Even then, this may overestimate the rate of real growth occurring, as there has been a trend of formalising much of the informal economy, for example child care, which is now a measured part of GDP rather than existing as individual family arrangements.

On these adjusted measures economic growth is a very slow process. In a world where non-renewable resource inputs are fixed or declining, it is the rate of the decline and the speed of adjustment that will determine the overall outcome for our well being. If the rate of decline of non-renewable resource inputs is below the rate of real growth (our ability to produce more with less) and the rate at which we can substitute to renewable alternatives, we can avoid economic calamity in the face of natural limits.

Unfortunately there are other factors at play.

The rate of population growth will greatly determine the per capita wellbeing in a time of limited growth. While extra labour input will no doubt contribute to production inputs, my suggestion is that this input will be outweighed by a decline in complementary resource inputs. Remember, we care about real economic ‘wealth’ per capita, and with more people there is a smaller share of remaining resources each person can utilise in production, thus reducing wellbeing.

Further, we can begin to take productivity gains as leisure time instead of more work time, thus there is a possibility of maintaining a given level of production in the economy with fewer labour inputs over time.

There is also the reliance of our financial system on high levels of growth. Many economic growth critics cite the need for exponential growth of financial measures of the economy as being in conflict with any finite system. Yet the ‘system’ itself is a human construction and I seen no reason why a stable money supply cannot operate under various levels of growth (even prolonged negative growth) if used cautiously and with little leverage.

Often forgotten is that many resources are currently fixed and yet go unnoticed. There are always 24 hours in a day, but that doesn’t stop us producing more each day. If a shortage of hours was encountered, would a sudden change to 23hrs (a 4% decline) have a dramatic impact? Or would society easily adjust to this new environment of tighter time scarcity?

While a smooth transition to prosperity under much greater limits on resource inputs to the economy is theoretically possible, I don’t expect this to be our future reality. Self interested governments, businesses and the general public will react to short term shocks in unexpected ways, potentially promoting conflict, and taking the bumpy road. I have no doubt that there will extended periods of prosperity in the future, but also expect a rough ride to get to them.

Cameron I'm impressed, there are some really good thoughts in this article, and you haven't shied away from discussing some of the "taboos" that enviromentalists traditionally sidestep.

ReplyDeleteI think that population growth, and the efficient management of all resources especially food and energy are going to be the most important subject in the century.

How do we in a mainly capitalist society make sure that all people have fair and reasonable access to food, shelter, education, and all other resources.

Do we need to alter our political system, do we need to put tax incentives in place to encourage a wider spread of use for our limited resources, how do we ramp up food production, provision of shelter, energy for lighting etc, online education facilities, the list goes on.

Excellent work, I'll give you an "A Plus"

Wow one post in glowing agreement from me appears to be a "kiss of death" for you Cameron, on what I thought would be a subject that touched a few nerves with some of your readers.

ReplyDeleteSorry...

Peter,

ReplyDeleteI actually had a nice reply written out but couldn't find the right words to sound humble and appreciative of your thoughts - but I definitely am. I think you would have clearly noticed my ideas mature over time, and I'm glad we see some common ground. In fact I think we have more common ground than is regularly revealed here because I try and blog on fringe ideas.

I also would have expected some argumentative replies, but have had nothing but support (here and on talkfinance). I guess shifting the mindset to see economic growth as a process of change and improvement, rather than and sum of output, leaves less to argue about.

Thanks Cameron. Yes you are growing in maturity every day, but please keep that random cannon loaded.

ReplyDeleteI don't visit sites that post predominitely bullish articles, they are usually trite sugar coated waffle, the economy is NEVER perfect, it has warts at the best of times.

I would much prefer to be challenged, so when I perform a dummy spit, it just means that you are doing your job well.

Cheers...

Not sure if I can agree with you here, Cam:

ReplyDelete"I need to be clear that when I talk of economic growth I mean our ability to produce more goods and services that we value for a given input."

There are some hard limits to efficiency gains(i.e. second law of thermodynamics).

An apple is still an apple no matter how you dice it. Cutting it with a progressively shaper and thinner blade might make the individual pieces progressively infinitesimally larger (rather than being left behind as juice or pulp on the chopping board etc.) up to a certain point but the total amount of apple remains fixed. It's a zero-sum game at the end of the day.

Of course, you could always finesse how you define economic growth, so that as time approaches infinity your efficiency gains approach zero, in which case you *would* have infinite growth. :-)

One thing that has to be taken into account is lead times in critical resource substitution. Plus the actual resources (labour, knowledge, energy, etc) required to changeover.

ReplyDeleteThese can range from quite quick to extremely long to infinite.

For example: switching to a low oil future takes considerable lead times and a massive new (and/or greatly expanded existing) infrastructure.

Putting in a sufficient rail infrastructure (plus the associated energy, maintenance, etc) to replace (say) 75% of car commuters, 90% of freight, 90% of air transport (a reasonable estimate of what would be required by about 2050 due to peak oil), would be considerable.

Now if this had been started a decade or more ago, then the annual cost would be quite acceptable. But, as we delay and delay, the annual cost for such a substitution gets greater and greater.

Leave it for too long and it becomes impossible as there is simply not enough spare resources to undertake it. And you would then get a economic/civilisation (as we now it) collapse sometime in the future.

This logic applies to any critical resource such as fossil fuel energy overall, certain irreplacable elements (e.g. phosphorus which would require putting in place a significant recycling infrastructure).

Plus positive feedback mechanisms come into play. The usual short term measure responding to greatly increased costs in critical resources and the recessions they inevitably create, is cutting cutting R&D, infrastructure investment, education, etc. Anything long term goes out the window as profits, taxes, incomes, etc become squeezed.

This brings some short term relief but actually brings forward the point of collapse.

So if you delay, you are faced with a series of shocks. Demand more and more often exceeds supply. Economic activity goes down, demand drops, cutbacks are made, demand creeps up again, another shock (now at a lower level) ... and so on. A downward death spiral in a series of firstly small shocks, but ever increasing at lower demand levels and shorter intervals.

Sadly typically the societal response is to dump more and more of the less influential (economically and politically) on the scrapheap, with initially a small proportion of society taking the largest hit. As time goes on this proportion grows and grows, until (if societal order has not collapsed by then) the vast majority are totally impoverished.

This is what is happening in the US and the UK today and there doesn't seem much chance of them avoiding a medium/long term collapse (ah lah the USSR).

Australia probably has about 5 years left (10 at the top) to avoid this future.

Hi

ReplyDeleteI don't know ... its just hard to envisage that an infinite growth can occur. Unless we are all going to live off world and move factorys off world and we therefore continue growth, but I think that's a long way off. I would feel that its hard not to see some hiatus in the climb to infinite value.

As I see it while 3rd world standards will rise this will require some dropping in standards of the "developed world" ... which I think we are already seeing.

but its a nice try

also:

ReplyDelete"A better measure of growth is real GDP per capita. "

I'm sorry but GDP is just such a lopsided view of things. I mean if I sell goods to my wife after I come home from the shopping and she sells me food that she serves on the table our house has not made more money.

it really is that simple

The problem with using econmics as the only tool is in omitting that it fails to measure what is important to humans, to quote Robert F Kennedy: "...the gross national product includes air pollution and advertising for cigarettes, and ambulances to clear our highway carnage. It counts special locks for our doors, and jails for the people who break them. The gross national product includes the destruction of the redwoods, and the death of Lake Superior. It grows with the production of napalm and missiles and nuclear warheads . . ."

ReplyDelete"And if the gross national product includes all this, there is much that it does not comprehend. It does not allow for the health of our families, the quality of their education or the joy of their play"

obakesan, I agree that most economic measures fail to capture what is important to people. But you know the saying "what gets measured gets managed". So better something than nothing.

ReplyDeleteYou are also right that an expansion of the formal economy, even if it is simply a replacement of the informal economy, is registered as growth, yet no new products or services have been provided.

There are plenty of people working hard to develop better measures of welfare - happiness indexes, new measures of progress etc, which combine economic hard data with other 'soft' survey data.

My point is that if we talk about growth in the purest of economic terms - satisfying human desires - we can continue to do better at this over time, even with diminishing non-renewable resources.

Hi

ReplyDeletethis part " we can continue to do better at this over time, even with diminishing non-renewable resources" I agree with fully. I just don't see "the dogma of infinite growth" as being based in reality ... unless we start living "off world"

There obviously can’t be any limit to growth, it’s all dependent upon person’s determination and passion, if these are the stuff that is present then it will never stop. I am extremely lucky that I work with OctaFX broker where they have got incredible facilities which gives helping me grow especially with their daily market updates, it’s really extra ordinary and make things lot easier for me, so that’s why I always prefer it and strongly believe that for success it’s necessary.

ReplyDelete